If you’ve ever stared at your bank app at 11 p.m. wondering where your paycheck went, you’re not alone — and honestly, the screen isn’t going to fix it.

That’s exactly why a budget binder is having such a moment in 2026. Cash stuffing videos are everywhere on TikTok, people are tired of swipe-happy spending, and a physical money system suddenly feels like the calmest, most grown-up thing you can do.

Here’s the thing: most beginner guides make it look complicated. Twenty tabs, fancy gold foil, hand-lettering you don’t have time for. Skip all that.

In this guide, I’ll walk you through how to build a simple, aesthetic budget binder from scratch — even if you’ve never budgeted a day in your life. You’ll learn the exact sections to include, what to leave out, how to set up cash envelopes that won’t tear, and the small design tricks that make you actually want to open the binder each week.

By the end, you’ll have a system that turns “where did my money go?” into “I know exactly where it went, and I planned it that way.” Let’s build yours.

Why a Budget Binder Beats Budgeting Apps (Especially in 2026)

Apps are convenient. They’re also frictionless — and that’s the problem.

When money moves with a tap, your brain barely registers it. A budget binder forces a pause: you have to open it, write it down, count cash, and physically move money between envelopes. That tiny bit of friction is what rewires spending habits.

Think of it like grocery shopping with a list versus shopping hungry without one. Same store, completely different outcome.

In 2026, more people are pulling away from screen-only finance for one reason: overspending is easier than ever, and the dopamine hit of “treat yourself” never ends. A physical budgeting binder turns money into something you can see and hold. According to Federal Reserve research on consumer payments, people consistently spend less when they pay with cash compared to cards — and a cash binder setup puts that psychology to work for you.

It’s not about being old-school. It’s about being intentional. And intentional is the new luxury.

→ Related: Simple Budget Plan for Beginners

What You Actually Need to Build a Budget Binder From Scratch

Before you order anything cute, breathe. You do not need a $90 leather portfolio to start. You need the basics, and you can upgrade later when you know what you’ll actually use.

Here’s the minimum starter kit:

- A 3-ring binder (1-inch is plenty for beginners; A6 size if you want a portable aesthetic)

- 10–15 clear zipper pouches or cash envelopes

- Tab dividers (5–8 sections)

- Loose-leaf paper or printable budget sheets

- A pen you actually like writing with (this matters more than people admit)

- Optional: washi tape, sticky tabs, a small calculator

That’s it. Total cost? Around $15–$30 if you grab everything from a discount store or Amazon. If you already have a binder lying around, even cheaper.

Don’t sleep on the pen, by the way. If your pen scratches, smudges, or runs out, you’ll quietly stop opening your binder. I’ve seen it happen.

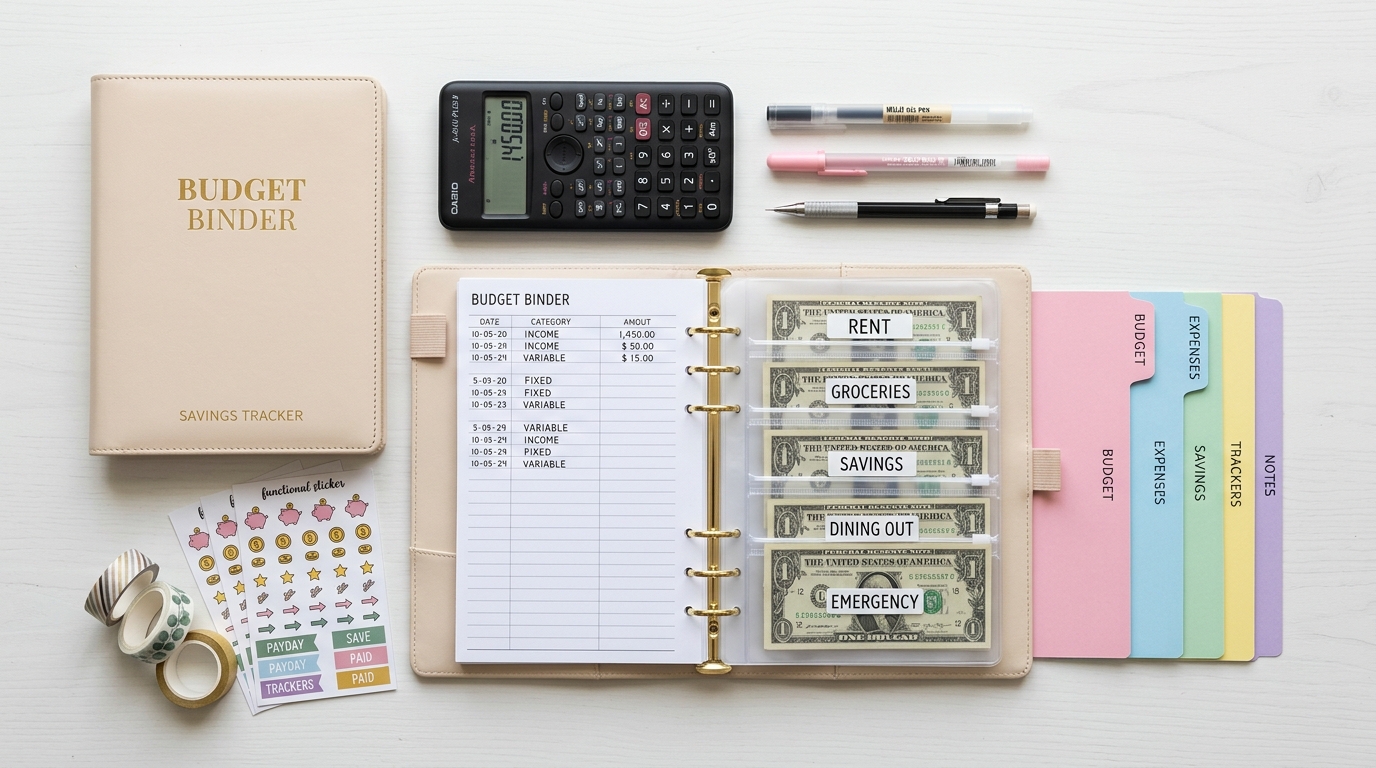

The 7 Essential Sections Every Beginner Budget Binder Needs

This is the part most guides overcomplicate. You don’t need 20 tabs. You need seven sections that cover 95% of your financial life.

1. Monthly Overview — A single page showing income, fixed bills, savings goals, and “fun money” for the month. This is your dashboard.

2. Bill Tracker — A simple list of every recurring bill, the due date, and a checkbox once it’s paid. Streaming subscriptions go here too (you’ll be surprised).

3. Cash Envelopes — One pouch per spending category: groceries, gas, dining, personal care, fun, etc. This is the heart of your cash envelope binder.

4. Savings Goals — One page per goal, with a visual tracker (a thermometer drawing, a coloring grid, anything you’ll fill in).

5. Sinking Funds — For irregular expenses you know are coming: car registration, birthdays, holidays, vet visits. These prevent emergencies that aren’t actually emergencies.

6. Debt Payoff — If you have debt, one page per balance with a payoff tracker. Watching numbers shrink is shockingly motivating.

7. Net Worth & Reflection — A simple monthly snapshot of assets minus debts, plus a short journaling space: what worked, what didn’t, what to adjust.

That’s the whole structure. Anything beyond these seven is bonus.

How to Set Up Your Cash Envelope Binder (Step by Step)

Now the fun part — actually building it. Grab your supplies and follow these steps in order. It’ll take about 90 minutes the first time.

Step 1: Decide your categories. Look at your last two bank statements and group spending into 6–10 categories. Be honest. If “DoorDash” deserves its own envelope, give it one.

Step 2: Set a cash amount per category. Add up what you realistically spent last month, then trim 10–15% off each category as your new target. Don’t slash everything in half — you’ll fail by week two.

Step 3: Label your envelopes. Use washi tape or a label maker for a clean look. Front of envelope = category name. Back = the monthly budget for that category. Done.

Step 4: Withdraw your cash. On payday, pull out the total cash you’ve assigned to envelopes. Use exact bills when possible (5s, 10s, and 20s make change easier).

Step 5: Stuff the envelopes. This is the satisfying part. Count out each amount and slip it into its pouch. A real-life example: my friend Priya started with $200 in her grocery envelope and finished the first month with $32 left — money she’d never have noticed in a bank app. She moved it straight to her vacation sinking fund.

Step 6: Use cash for those categories all month. When an envelope is empty, that category is closed until next month. No “borrowing” from other envelopes — that breaks the system.

Step 7: Review on the last day of the month. Empty every envelope, count what’s left, log it in your monthly overview, and decide where leftovers go (savings, debt, rolling over). Then start fresh.

Budgeting Binder Ideas That Make It Actually Aesthetic

Let’s be real — if your binder looks like a tax document, you’ll avoid it. Aesthetics aren’t shallow here. They’re a retention strategy.

A few low-effort upgrades that make a huge difference:

- Pick a color palette and stick to it. Two or three colors max. Sage green + cream + black is foolproof. So is dusty pink + tan + white.

- Use one font family. If you’re printing pages, one clean sans-serif (think Poppins or Inter) keeps things calm.

- Add a cover page. Even a simple “My 2026 Money Plan” in nice typography makes the binder feel personal.

- Insert one inspiration page. A photo of your savings goal — the apartment, the trip, the debt-free life — taped on the inside front cover. You’ll see it every time you open up.

- Use clear page protectors. They keep your printables crisp and let you reuse trackers with a dry-erase marker.

Want plug-and-play visuals? You can find free budget binder printables on Pinterest by searching “minimalist budget binder printables 2026” — pick one designer whose style you love and use their full set so everything matches.

The goal isn’t to make a museum piece. It’s to make something you don’t dread opening on a Sunday evening.

5 Beginner Budget Binder Mistakes to Avoid

I’ve watched a lot of people start strong and quit by week three. Almost every time, it’s one of these mistakes:

Mistake 1: Too many categories. Twelve envelopes sounds organized, but it’s exhausting. Start with 6–8. Add more only if a category keeps spilling over.

Mistake 2: Unrealistic amounts. If you spent $600 on groceries last month, don’t budget $300 this month and call it discipline. That’s a setup for failure. Trim slowly.

Mistake 3: Skipping sinking funds. Without them, every car repair becomes a crisis. Even $20 a month into a “car stuff” envelope changes everything.

Mistake 4: Not tracking irregular income. If you freelance, do gig work, or get tips, your binder needs an income log too. Average your last three months to set a baseline.

Mistake 5: Treating it as all-or-nothing. Missed a week? Spent from the wrong envelope? Don’t burn it down. Adjust and keep going. The people who win at budgeting are the ones who keep showing up imperfectly.

The point isn’t a perfect month. It’s a clear one.

DIY Budget Binder Printables: Make Your Own in Under an Hour

You don’t need design skills to make your own pages. Open Canva (free), search “budget planner template,” and you’ll find dozens you can edit in minutes.

What to create:

- A monthly overview page (income, expenses, savings, notes)

- A weekly spending log

- A bill tracker with due-date checkboxes

- A savings goal tracker with a fillable progress bar

- A debt payoff sheet

- A sinking funds tracker

Save them as PDFs, print double-sided to save paper, and hole-punch them into your binder. The whole process takes 45–60 minutes and gives you a fully custom money organizer binder for 2026 that fits how you actually think about money — not how some template says you should.

Pro tip: print extras. You’ll mess up. You’ll change categories in February. Having a stack ready means you won’t quit over a paperwork problem.

Final Thoughts: Your Budget Binder Is a Tool, Not a Test

Remember that 11 p.m. bank app moment from the start? That feeling fades faster than you’d think once you have a system that actually shows you where the money goes.

A budget binder isn’t about being frugal, restrictive, or boring. It’s about making invisible money visible — turning a flood of taps and swipes into something you can see, count, and decide about. That’s where control comes from.

You don’t have to build the perfect binder this weekend. Pick a binder, label five envelopes, and start with this month’s grocery and gas budgets. That’s it. The rest comes naturally as you go.

The people who feel “good with money” aren’t smarter or richer — they just have a system they trust. Now you have one too.

If you want to go deeper, Loud Budgeting Explained is the perfect next step.

Save this post, share it with the friend who keeps texting “how are you so on top of your bills?”, and start your binder today. Future you is already thanking you.

Frequently Asked Questions

Q: How much money should I keep in a budget binder?

Only the cash you’ve assigned to your monthly envelopes — typically $200–$800 depending on your variable expenses. Keep fixed bills (rent, utilities, subscriptions) on autopay from your bank account, and never store large amounts of cash in your binder. Treat it like a working wallet, not a savings vault.

Q: Is a budget binder better than a budgeting app?

For people who overspend, yes — the physical friction of counting cash and writing things down slows impulse purchases in a way apps can’t. That said, plenty of people use both: a binder for daily spending categories and an app for tracking net worth and investments. Use whatever you’ll actually open every week.

Q: Can I start a budget binder if I have irregular income?

Absolutely, and a binder might suit you better than an app. Average your last three months of income to set a realistic monthly baseline, then build your envelopes off that lower number. Any income above the baseline goes straight into a “buffer” envelope so leaner months don’t derail you.