If you’ve been searching for a simple budget plan for beginners, you’re already ahead of most people — because most people never start. According to a 2024 survey by Bankrate, nearly 73% of Americans feel financially stressed, and a significant part of that stress comes from simply not knowing where their money goes each month.

Here’s the truth: you don’t need a finance degree, a complicated spreadsheet, or a six-figure salary to get your finances under control. Moreover, creating a workable personal budget doesn’t take more than an hour the first time. What it does take is a clear framework, a little honesty, and the willingness to start — even imperfectly.

Throughout this guide, you’ll find a step-by-step breakdown of how to build your first monthly budget, choose the right budgeting method, set up spending categories, and actually stick with it over time. By the end, you’ll have everything you need to create a simple budget plan for beginners that fits your real life — not some idealized version of it.

Why Every Beginner Needs a Simple Budget Plan

Before diving into the steps, it’s worth taking a moment to understand the “why” — because knowing the purpose makes the process stick far longer than discipline alone.

A budget, at its core, is not a restriction. Rather, it’s a decision made in advance about where your money goes. Instead of wondering at month’s end where everything disappeared, you direct it intentionally. Furthermore, a simple budget plan for beginners gives you financial clarity — and clarity leads to better decisions without requiring guilt or superhuman willpower.

Consider this: if you earn $4,000 a month and spend $4,200, you’re slowly falling behind without realizing it. However, if you know precisely that $1,400 goes to rent, $500 to groceries, $300 to your car, and $200 to streaming subscriptions you barely watch — suddenly you can make real choices. You might cancel two services, redirect that $200 toward savings, and feel no meaningful drop in quality of life.

That shift in awareness is what changes financial trajectories.

📷 IMAGE PLACEHOLDER 2 File name: why-budget-matters-beginners.jpg Alt text: beginner budget plan chart showing income versus expenses breakdown on paper Caption: A beginner budget plan helps you see exactly where your money goes — and where to redirect it.

The Real Cost of Skipping a Budget

Here’s a sobering statistic from the Federal Reserve’s 2023 Report on Economic Well-Being: 37% of American adults couldn’t cover an unexpected $400 expense without borrowing money or selling something. Notably, that figure cuts across income brackets — it’s frequently not a low-income problem. Instead, for many households, it’s a planning problem.

When there’s no budget in place, most people tend to:

- Overspend on things that don’t truly matter to them

- Underspend on the things that actually do

- Accumulate debt gradually and often without realizing it

- Feel financially anxious even when their income is perfectly reasonable

Fortunately, a simple budget plan for beginners addresses all of these problems — and it doesn’t need to be complicated to be effective.

Step 1: Calculate Your Real Monthly Income

This step sounds obvious, yet surprisingly many beginners either skip it or get it wrong. Your income isn’t your annual salary — it’s the net amount that actually lands in your bank account after taxes and deductions.

How to Find Your True Take-Home Pay

If you’re a salaried employee in the US, your most recent pay stub is the right place to start. Specifically, look for the line labeled “net pay” — that’s what you actually take home after federal and state taxes, Social Security, Medicare, and any pre-tax deductions like health insurance or 401(k) contributions.

For example:

- Gross salary: $55,000/year (~$4,583/month)

- After federal/state taxes, Social Security, and health insurance deductions: approximately $3,400/month

That $3,400 is your real baseline — and consequently, that’s the number your budget must work within.

What If Your Income Varies Each Month?

Freelancers, gig workers, and part-time employees often deal with unpredictable paychecks, which makes budgeting feel significantly harder. In that case, a reliable strategy is to use your lowest-earning month from the past six months as your planning baseline. That way, you’re never counting on money that might not arrive.

Additionally, treat higher-income months as an opportunity — rather than spending more freely, funnel the extra toward your savings goals or emergency fund. This approach, sometimes called “income flooring,” provides real stability even when earnings fluctuate from week to week.

🔗 INTERNAL LINK: Link “emergency fund” → How to Build an Emergency Fund Fast

Step 2: List Every Expense Honestly

This is the step most people quietly dread — because it means confronting spending habits they’d rather not examine. That’s completely understandable, so think of this as a fact-finding mission rather than a judgment session.

The goal is simple: capture every dollar that leaves your account in a typical month.

Fixed Expenses — The Predictable Ones

Start with the bills that are identical every month, since these are easiest to document:

- Rent or mortgage payment

- Car loan or lease payment

- Student loan minimums

- Health, auto, and renters/homeowners insurance

- Phone bill

- Internet service

- Monthly subscriptions (gym, apps, streaming)

Write down the exact amounts. These are generally non-negotiable in the short term, so treat them as locked entries in your simple budget plan.

Variable Expenses — Where Most Budgets Get Fuzzy

Variable expenses shift from month to month, which is precisely why they’re harder to track accurately. Common examples include:

- Groceries

- Gas or public transportation

- Dining out and takeout

- Clothing and personal care

- Entertainment and hobbies

- Online shopping

- Gifts and celebrations

For these categories, review your bank or credit card statements from the past two to three months and calculate a realistic average for each. Be accurate rather than optimistic — the numbers you gather here directly determine whether your budget actually holds up in practice.

Irregular Expenses — The Hidden Budget Killers

Here’s what catches even well-intentioned budgeters off guard: expenses that don’t arrive every month but reliably show up every year. These include things like:

- Car registration and maintenance

- Annual software or subscription renewals

- Holiday and birthday shopping

- Medical copays and dental visits

- Home repairs and appliance replacements

The solution is to total these costs annually, then divide by 12. That monthly contribution needs a dedicated spot in your budget — even in months when the actual bill isn’t due. Without this, entirely predictable costs feel like surprises, and surprises are what derail otherwise solid plans.

Step 3: Choose the Right Beginner Budgeting Method

One of the most common mistakes people make when building a simple budget plan for beginners is choosing a method that doesn’t match their personality. As a result, the system feels impossible to maintain, and they abandon it within a few weeks. Here are three beginner-friendly methods — each with different strengths.

📷 IMAGE PLACEHOLDER 3 File name: budgeting-methods-comparison-beginners.jpg Alt text: simple budget plan for beginners comparison chart showing 50/30/20 rule zero-based and pay yourself first methods Caption: Choosing the right method is essential to building a simple budget plan for beginners that actually sticks.

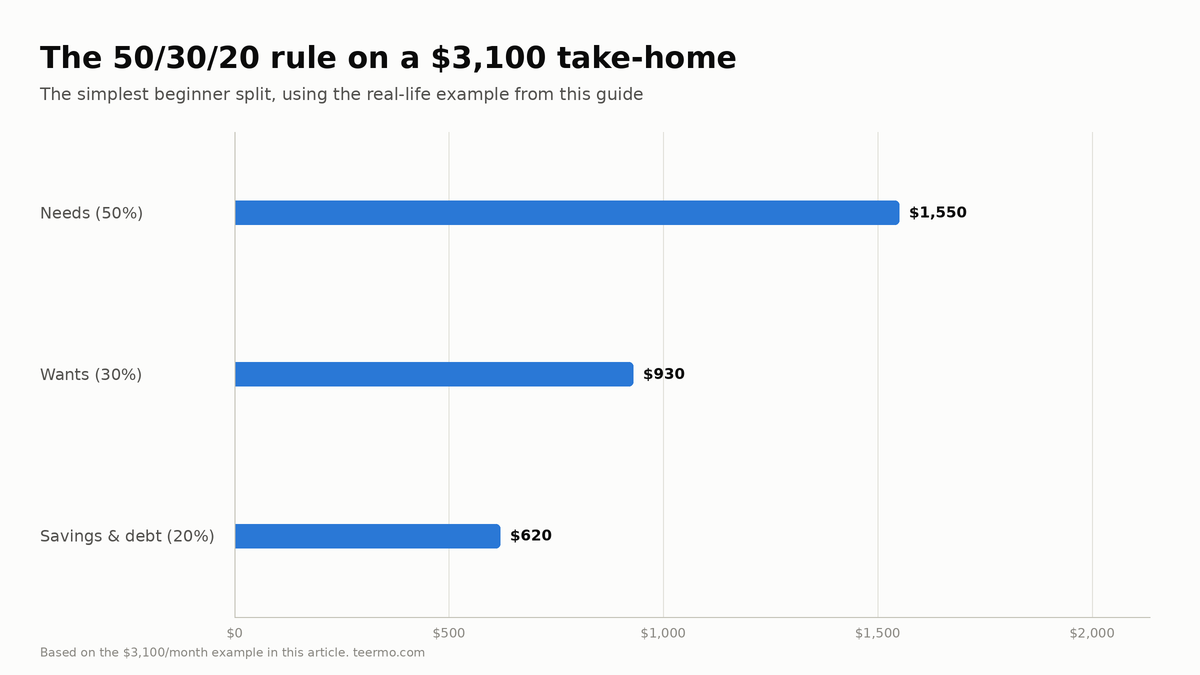

The 50/30/20 Rule — The Simplest Budget Plan for Most Beginners

The 50/30/20 rule is widely considered the most beginner-friendly budgeting framework because it’s easy to remember and requires minimal day-to-day tracking.

Here’s how it divides your take-home pay:

- 50% → Needs: Rent, groceries, utilities, insurance, minimum debt payments

- 30% → Wants: Dining out, entertainment, travel, hobbies, subscriptions

- 20% → Savings and Debt Payoff: Emergency fund, retirement contributions, extra loan payments

Practical example using $3,400/month take-home:

- Needs: $1,700

- Wants: $1,020

- Savings/Debt: $680

This method works well because it provides structure without micromanaging every single transaction. However, if you live in a high cost-of-living city like New York, Los Angeles, or Seattle, fitting needs under 50% can be genuinely difficult. In that case, adjust the ratios — for example, 60% needs, 20% wants, and 20% savings — to reflect your actual reality.

Zero-Based Budgeting — Best for Beginners Who Want Full Control

In zero-based budgeting, every dollar of income is assigned a specific job so that income minus expenses equals exactly zero at the end of the month. Importantly, you’re not spending everything — you’re also assigning dollars to savings and debt payoff.

How it works step by step:

- Write down your total monthly take-home income

- List every expense, savings goal, and debt payment

- Adjust allocations until income minus expenses equals zero

This method provides the most granular control over your money, particularly if you’re actively paying down debt or have variable spending patterns. Apps like YNAB (You Need a Budget) are specifically built around this framework.

The Pay-Yourself-First Method — Best for People Who Struggle to Save

This approach flips the conventional order of operations. Instead of spending first and saving whatever remains (which is typically nothing), you transfer your savings target to a separate account the moment your paycheck arrives — before a single bill is paid.

From there, you spend the rest as your needs require. Additionally, this method removes the friction of saving because the decision is made automatically. A practical starting point is 10% of take-home pay; however, even $50 or $100 per month is enough to establish the habit, which matters more than the specific dollar amount in the beginning.

Step 4: Set Up Budget Categories for Your Personal Plan

Once you’ve selected a method, the next step in your simple budget plan for beginners is building the actual category structure. Below is a practical starter template designed for US households:

Housing

- Rent or mortgage

- Renter’s or homeowner’s insurance

- Utilities (electric, gas, water)

- Internet and streaming services

Transportation

- Car payment or lease

- Gas and fuel

- Auto insurance

- Parking, tolls, or public transit fares

Food and Dining

- Groceries

- Dining out and takeout

- Coffee and snacks purchased outside the home

Health and Wellness

- Health insurance premiums (if not deducted from your paycheck)

- Prescription medications and copays

- Gym or fitness membership

Personal and Lifestyle

- Clothing

- Personal care products and services

- Hobbies and recreation

- Subscriptions (Netflix, Spotify, apps)

Financial Goals

- Emergency fund contributions

- Retirement savings (Roth IRA, 401k contributions beyond your employer match)

- Extra debt payoff above required minimums

- Specific savings goal (vacation, new car, home down payment)

Sinking Funds

- Car maintenance and repairs

- Medical and dental out-of-pocket costs

- Gifts and holiday spending

- Annual subscription renewals

Don’t worry about getting the categories perfectly right on the first try. Furthermore, the most important principle is that every dollar has a designated home — because unassigned money tends to disappear.

🔗 INTERNAL LINK: Link “Roth IRA” → Roth IRA vs Traditional IRA: Which Is Right for You?

Step 5: Run the Numbers and Close the Gap

With your income documented and expenses categorized, it’s time to compare the two numbers. Add up all monthly expenses and subtract that total from your take-home pay.

If Your Simple Budget Plan Shows a Surplus

If your expenses are less than your income — great. Now, rather than letting that surplus drift into your checking account where it’ll disappear quietly, assign it a specific job immediately. Specifically, consider boosting your emergency fund, making an extra debt payment, or moving it into a high-yield savings account.

As of 2025, many online high-yield savings accounts are offering approximately 4.5–5% APY — dramatically higher than the national average of 0.06% at traditional brick-and-mortar banks. That difference compounds meaningfully over time without requiring any additional effort on your part.

If Your Expenses Exceed Your Income

This situation calls for honest assessment. If you’re spending more than you earn each month, you have two levers available: reduce expenses or increase income. In practice, most people benefit from doing a bit of both.

To reduce spending, start with these:

- Cancel subscriptions you use fewer than twice per month

- Reduce dining-out frequency by even one or two meals per week

- Apply a 48-hour pause rule before any non-essential online purchase

- Switch to store brands where quality is genuinely comparable (often it is)

To increase income, consider these options:

- Requesting a raise — according to Payscale research, roughly 70% of employees who ask for raises with documented performance receive one

- Freelancing an existing skill on evenings or weekends

- Selling unused household items through Facebook Marketplace or eBay

- Taking on overtime hours or a short-term side gig

Step 6: Build Your Emergency Fund First

Before aggressively paying down debt or contributing heavily to investments, one priority stands above the rest in any simple budget plan for beginners: a starter emergency fund.

The conventional recommendation is three to six months of living expenses, but that target can feel overwhelming when you’re just getting started. Therefore, aim first for a milestone of $1,000. Most everyday financial emergencies — a flat tire, an urgent care visit, a broken appliance — fall within that range. Moreover, having even a small cash cushion means a difficult day doesn’t turn into a month of high-interest credit card debt.

Once you’ve saved $1,000, keep it in a separate savings account rather than your checking account — separation helps prevent accidental spending. After that initial buffer is in place, you can begin splitting your monthly savings between growing the emergency fund and pursuing other financial goals.

🔗 INTERNAL LINK: Link “high-interest credit card debt” → How to Pay Off Credit Card Debt Fast

Step 7: Track Your Spending — The Step That Makes Budgets Work

A common misconception among beginners is that creating a budget is a one-time task. In reality, however, a budget is a living system. You set it up once, then check in regularly to compare actual spending against your plan.

Beginner-Friendly Tools for Tracking Your Budget

You don’t need to record every transaction manually — several tools connect directly to your bank accounts and handle categorization automatically:

YNAB (You Need a Budget): Costs $14.99/month or $99/year, but it consistently earns top ratings from personal finance experts for its ability to genuinely change spending behavior. Most new users report saving well beyond the subscription cost within the first month of active use.

EveryDollar: Free basic version built around zero-based budgeting principles. The premium plan syncs directly with your bank for automatic transaction imports.

Credit Karma (formerly Mint): Free and easy to use, with automatic transaction categorization and a visual spending overview that works particularly well for people brand-new to budgeting.

A simple Google Sheet: Don’t underestimate this option. A spreadsheet with columns for category, budgeted amount, and actual spending is genuinely all that many people ever need — and it costs nothing.

The 10-Minute Weekly Budget Check-In

The single habit that separates people who succeed with their simple budget plan from those who abandon it after two months is a brief weekly review. Specifically, spending just 10 minutes each week comparing current spending against your budget allows you to course-correct while there’s still time left in the month — rather than discovering the full extent of overspending on day 30.

Step 8: Adjust Your Budget — Don’t Abandon It

Here’s something nobody tells you when you first build a simple budget plan for beginners: your first attempt will almost certainly be inaccurate. Not dramatically wrong — but imprecise enough that some categories run dry by the 20th and others have money sitting untouched.

That is entirely expected. In fact, it’s also the most important part of the learning process.

The most common mistake at this stage is treating a blown budget as a personal failure and walking away from the whole effort. Instead, treat the overage as useful data. If grocery spending consistently exceeds your estimate, the estimate was probably too low — not your willpower too weak. Similarly, if money sits unused in your dining-out category every month, redirect that surplus to savings or debt payoff instead of leaving it idle.

Budget reviews are course corrections, not confessions. Athletes watch game film. Writers revise drafts. In the same way, budgeters review numbers and adjust allocations. That’s not failure — it’s the system working exactly as it should.

When to Fully Revisit Your Budget Plan

Beyond monthly check-ins, any major life change should trigger a complete budget review:

- New job, raise, or reduction in income

- Moving to a new home or city

- Adding or losing a household member

- Getting married or going through a divorce

- Taking on significant new debt

- Paying off an existing loan

- A notable change in health or medical expenses

Your budget should always reflect your current circumstances — not the financial situation you had six months ago.

Common Mistakes Beginners Make With Budget Plans

Even with the best intentions, beginners tend to run into the same predictable pitfalls. Fortunately, all of them are entirely avoidable once you know what to look for.

Mistake 1: Forgetting Irregular Expenses

As covered earlier, irregular expenses are among the top reasons a simple budget plan for beginners falls apart in the first three months. The fix is straightforward: create dedicated sinking fund categories and contribute to them monthly, even when the bill isn’t due yet.

Mistake 2: Making the Budget Too Restrictive

A budget that feels like punishment simply won’t last. Therefore, always build in a “fun money” or “guilt-free spending” line item — even just $30 to $50 per month. That small release valve makes the entire system more sustainable and psychologically manageable over the long term.

Mistake 3: Not Aligning With Your Partner

If you share finances with a spouse or partner, building a budget without their involvement will eventually create friction. Money conversations are uncomfortable, but they’re far less painful than the resentment that accumulates when one person feels blindsided or controlled.

Consider scheduling a monthly “money meeting” — even 30 minutes over coffee — to review spending and align on shared goals. Research consistently shows that couples who communicate openly about finances report both higher savings rates and greater relationship satisfaction overall.

Mistake 4: Waiting for the Perfect Moment to Start

There’s no ideal month to begin a simple budget plan for beginners. Not after the holidays. Not after the next raise arrives. Not when life settles down. The right time to start is always now — with your current income, your current expenses, and whatever imperfect information you have available today.

Start. Adjust as you go. Improve steadily over time. That’s the complete system.

A Real-Life Beginner Budget Example

To bring everything together, here’s a realistic example. Meet Jordan — a 26-year-old living in Columbus, Ohio, earning $47,000/year before taxes.

Jordan’s Monthly Take-Home Pay: ~$3,100

| Category | Budgeted Amount |

|---|---|

| Rent (1BR apartment) | $875 |

| Utilities + Internet | $125 |

| Groceries | $280 |

| Dining Out | $140 |

| Gas | $75 |

| Car Insurance | $92 |

| Phone Bill | $65 |

| Subscriptions | $38 |

| Personal Care | $50 |

| Clothing | $40 |

| Entertainment | $70 |

| Emergency Fund | $200 |

| Roth IRA | $100 |

| Sinking Funds (car, medical, gifts) | $80 |

| Miscellaneous | $40 |

| Total Allocated | $2,270 |

| Surplus (applied to student loans) | $830 |

Jordan’s simple budget plan took about three months of adjustments before the grocery and dining-out figures felt genuinely realistic. Nevertheless, it works — and that $830 monthly surplus is going directly toward eliminating student loan debt ahead of schedule.

That’s what a working beginner budget looks like: not perfect, but functional and consistently improving.

📷 IMAGE PLACEHOLDER 4 File name: beginner-budget-example-table.jpg Alt text: example simple budget plan for beginners showing monthly categories and dollar amounts in a spreadsheet Caption: A sample simple budget plan for beginners showing how a $3,100 monthly income can be effectively allocated.

Frequently Asked Questions About Simple Budget Plans for Beginners

Q: What is the simplest budget plan for beginners to start with?

A: The 50/30/20 rule is widely regarded as the easiest starting point for people new to budgeting. It divides your take-home pay into three categories: 50% for needs like rent and groceries, 30% for wants like dining out and entertainment, and 20% for savings and debt repayment. Because it uses broad buckets rather than detailed line-item tracking, it’s straightforward to implement without feeling overwhelming or restrictive.

Q: How much of my income should I save each month as a beginner?

A: A commonly recommended starting target is 20% of take-home pay, though even 5–10% is a meaningful beginning if your budget is currently tight. What matters most in the early stages is building the habit consistently rather than hitting a specific dollar amount. As you pay off debts and your income grows over time, you can gradually increase your savings rate. Many certified financial planners suggest working toward a combined savings rate of 15–20% — including retirement contributions — as a longer-term benchmark.

Q: Do I need a budgeting app, or will a simple spreadsheet work?

A: Either approach works effectively — the most important factor is using whatever tool you’ll return to consistently. Apps like YNAB and EveryDollar simplify tracking by automatically syncing with your bank accounts. However, a Google Sheet with columns for category, budgeted amount, and actual spending is equally effective for people who prefer a manual, hands-on approach. The technology itself is secondary; the habit of reviewing your numbers regularly is what drives lasting results.

Q: What should I do if I go over budget in a category?

A: First and foremost, don’t treat it as a failure — overspending in individual categories happens to experienced budgeters regularly. Review whether any other categories have remaining funds you can temporarily redirect. If you consistently overspend in the same area month after month, that’s a signal to raise your budget allocation rather than repeat the same shortfall indefinitely. Additionally, examine whether the root cause is a behavioral pattern or an unrealistic original estimate — because the fix looks different depending on which one it is.

Q: Is a simple budget plan worth building if I’m already living paycheck to paycheck?

A: Especially in that situation, yes — without question. A budget won’t create money that isn’t there, but it will ensure every dollar you do have works as efficiently as possible rather than leaking out without direction. Moreover, many people in tight financial situations discover through budgeting that small adjustments — a cancelled subscription here, one fewer restaurant meal there — collectively create just enough breathing room to start a small emergency fund. That first $200 or $500 in savings changes the psychological experience of money in a genuinely meaningful way, even before the numbers look dramatically better on paper.

Final Thoughts: Start Your Simple Budget Plan for Beginners Today

The most important thing to understand about budgeting — particularly if you’re just beginning — is that it isn’t a measure of your discipline, intelligence, or financial worth. Rather, it’s a practical tool. A flexible, adjustable, imperfect tool that helps you move your money in the direction of the life you actually want to live.

You don’t need to execute it perfectly on the first try. Instead, you simply need to start, stay curious when something doesn’t work as expected, and come back to it month after month. Over time, that consistency compounds into something genuinely significant — not only in your bank account balance, but in how you feel about money every single day.

The people who build lasting financial stability aren’t necessarily the highest earners. Rather, they’re the ones who know what they have, know where it’s going, and make deliberate choices about both. A simple budget plan for beginners is precisely what makes that possible — and today is the right time to build yours.

This article is intended for general educational purposes and reflects personal finance practices common in the United States. It is not a substitute for personalized advice from a certified financial planner (CFP) or licensed financial advisor.