You check your bank app on a Tuesday morning and feel that familiar stomach drop. Where did the money go? You didn’t even do anything fun. Just a few “small” Target runs, two food delivery orders, and one impulse Amazon checkout at 11 p.m. Sound familiar?

You’re not bad with money. You’re just budgeting blind.

That’s exactly why the envelope budgeting method is exploding again in 2026. With rent, groceries, and gas all climbing, people are ditching invisible debit-card spending and going back to a system you can literally hold in your hands. It’s tactile, brutally honest, and impossible to “accidentally” overspend with.

In this guide, I’ll walk you through the envelope budgeting method step by step — the way I’d explain it to a friend over coffee, not a finance textbook. No jargon, no shame, no “spend less on lattes” lectures. Just a clear system that turns your paycheck into a plan, your spending into a habit, and your money stress into something rare and beautiful: control.

What Is the Envelope Budgeting Method, Really?

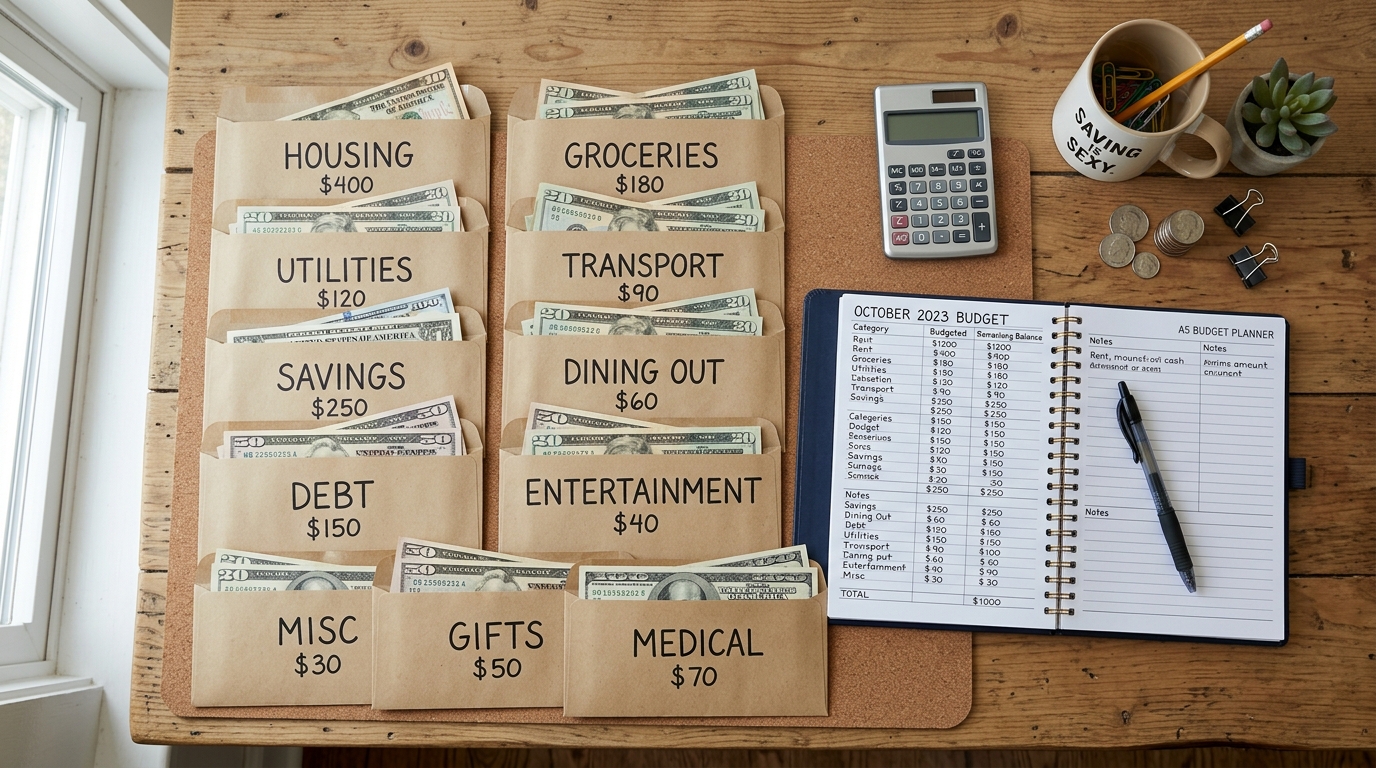

The envelope budgeting method is a cash-based system where you divide your monthly income into spending categories — and put a set amount of physical cash into a separate envelope for each one. When the envelope is empty, you stop spending in that category. That’s it. That’s the whole thing.

It sounds almost too simple. But that simplicity is the secret weapon.

Your brain processes cash differently than tapping a card. Research from professors at MIT and Carnegie Mellon found that people are willing to pay significantly more when using credit cards versus cash — sometimes nearly double. Cash hurts a little to hand over, and that tiny ache is exactly what stops mindless spending.

Think of each envelope as a tiny budget bouncer. It doesn’t argue. It doesn’t negotiate. When the cash is gone, the party’s over until next month.

Now in 2026, plenty of people use a hybrid version — physical envelopes for some categories, digital “envelopes” inside budgeting apps for others. Both count. The principle is what matters: every dollar gets a job before the month starts.

If you’re brand new to budgeting, our zero-based budgeting guide explains how to give every dollar a job — the same philosophy that makes envelopes so effective.

Why the Envelope System Budget Works When Apps Don’t

You’ve probably tried a budgeting app. Maybe two. You downloaded it on a hopeful Sunday, linked your accounts, and… stopped opening it by Wednesday.

Here’s the thing: apps show you what you spent after you spent it. The envelope system budget shows you what you have before you spend. That’s not a small difference — it’s the entire difference between reacting and deciding.

When you can see three twenties left in your “Groceries” envelope on the 22nd of the month, you make a different choice at Trader Joe’s. You skip the fancy cheese. You grab the store-brand pasta. You leave with what you needed.

Try doing that with a number on a screen you have to remember to check.

There’s also the dopamine angle. Filling envelopes at the start of the month feels weirdly satisfying — like organizing a junk drawer or finishing a to-do list. It gives budgeting an emotional payoff most people never get from spreadsheets.

The envelope system works because it turns a willpower problem into a logistics problem — and logistics is way easier to win.

Cash Envelope Categories: What to Actually Include

Pick the wrong categories and the whole system collapses by week two. Pick the right ones and it almost runs itself. Here are the cash envelope categories most beginners should start with — keep it under eight to avoid envelope fatigue.

Essential variable categories (use cash envelopes):

- Groceries — the biggest leak for most households

- Gas / Transportation — fluctuates monthly, perfect for envelopes

- Eating Out / Coffee — where “small” purchases bleed budgets dry

- Personal Care — haircuts, skincare, drugstore runs

- Entertainment / Fun Money — non-negotiable; budgets without fun money fail

- Household Supplies — paper towels, cleaning stuff, the “Target $5 items”

- Clothing — even if it’s small, it deserves its own envelope

- Gifts / Misc — birthdays sneak up on everyone

Skip these for envelopes (pay them digitally instead): rent, mortgage, utilities, insurance, subscriptions, debt payments. These are fixed bills — putting them in cash envelopes is just extra work.

A friend of mine — let’s call her Jess — started with twelve envelopes because she wanted to be “thorough.” She gave up in 11 days. We rebuilt her system with six envelopes and she’s been running it for over a year now. Fewer envelopes, more discipline. Always.

According to a Bankrate survey on American budgeting habits, more than half of U.S. adults don’t follow a written budget — and overspending on food and discretionary categories is the #1 reason budgets fail. Those are exactly the categories envelopes fix.

The Envelope Method: How To Get Started in 9 Steps

Ready to actually do this? Here’s the envelope method how to — the full step-by-step. Don’t skip steps. Each one matters.

Step 1: Calculate your real monthly take-home pay.

Not your salary. Your actual deposit after taxes, insurance, and 401(k). If your income varies, use your lowest month from the last three. Plan for the floor, not the ceiling.

Step 2: List every fixed bill first.

Rent, utilities, insurance, minimum debt payments, subscriptions. Subtract these from your take-home. Whatever’s left is what you actually have to work with — and it’s usually less than you think.

Step 3: Choose 5–8 cash envelope categories.

Use the list above. Resist the urge to make 14 envelopes. The envelope budgeting method rewards simplicity, not perfection.

Step 4: Assign a dollar amount to each envelope.

Look at your last two months of actual spending in each category — not what you wish you spent. Be honest. If you spent $620 on groceries last month and you set the envelope to $300, you’re setting yourself up to fail by the 12th.

Step 5: Withdraw the cash on payday.

Go to the bank or ATM the same day you get paid. This is the whole game — if the cash stays in your checking account, your debit card will find a way to spend it.

Step 6: Physically fill and label each envelope.

Write the category name and the amount on the front. Some people add the date. The act of writing it makes it feel real.

Step 7: Only spend from the envelope for that category.

This is the rule everyone wants to bend in week one. Don’t. If “Eating Out” is empty on the 19th, you cook at home until the 1st. That’s the discipline that creates the freedom.

Step 8: If an envelope empties early, do NOT raid another one.

This is the #1 beginner mistake. Either the budget needs adjusting next month, or you needed to slow down this month. Both lessons are valuable. Stealing from “Gas” to pay for sushi is how the whole system unravels.

Step 9: At month-end, review what’s left over and decide.

Leftover cash from a tight category? Roll it into next month’s envelope, transfer it to savings, or send it to debt. Whatever you do, don’t just spend it because it’s there. The whole point of beginner envelope budgeting is replacing autopilot with intention.

5 Mistakes That Quietly Kill the Cash Budgeting System

I’ve watched dozens of people try this system. The ones who quit almost always make the same handful of mistakes. Spot them now, dodge them later.

Mistake 1: Too many envelopes. Twelve categories sound organized. They’re not — they’re exhausting. Start with five or six.

Mistake 2: Underfunding “fun money” to zero. A budget with no joy in it is a diet with no carbs. You’ll binge by week two. Give yourself a small, guilt-free amount.

Mistake 3: Refusing to adjust. Your first month’s amounts will be wrong. That’s normal. Adjust the numbers next month — don’t abandon the whole system.

Mistake 4: Keeping all envelopes in your wallet. That’s how cash “mysteriously” disappears. Keep most envelopes at home; only carry the one you’ll use that day.

Mistake 5: Ignoring irregular expenses. Car registration, gifts, annual subscriptions — these don’t happen monthly but they happen. Add a small sinking fund envelope so they never blindside you.

Quick honesty check: have you done any of these? I have. Twice. The system isn’t broken — it just needs tweaking, and that’s part of the process.

Money Envelope System 2026: How It’s Changing (And Why It’s Booming)

The money envelope system in 2026 doesn’t look exactly like your grandmother’s. Some people still use real cash and real envelopes — the cash stuffing trend on TikTok has nearly a billion views and shows no sign of slowing. Others use hybrid systems with apps like Goodbudget, YNAB, or Monarch that mimic envelopes digitally.

Both work. The principle is what matters: predecided money, divided into purpose-driven buckets, with hard limits.

What’s driving the boom? Three things.

Living costs jumped hard between 2022 and 2025, and people who used to “feel okay” financially suddenly didn’t. Vague budgeting stopped cutting it.

Second, the dopamine fatigue of digital everything has people craving tactile, slow, intentional habits. Cash stuffing scratches the same itch as journaling or meal-prepping on Sunday — it feels grounding.

Third, social media made the method visible. When you see someone fold a stack of twenties into a “Groceries” envelope on video, the abstract idea of “budgeting” suddenly looks doable. Doable beats perfect every time.

Whether you go full-cash or hybrid, the envelope budgeting method works in 2026 for the same reason it worked in 1956: it makes invisible money visible.

Final Thoughts: The Real Reason This Method Changes People

Remember that stomach drop from the beginning — checking your account and not knowing where it all went? The envelope budgeting method makes that feeling almost impossible.

Not because you’ll be perfect. You won’t. Some month, you’ll overspend on groceries or “borrow” from the wrong envelope and feel a little defeated. That’s not failure. That’s data.

The deeper shift is psychological. You stop being the person money happens to and become the person who tells money where to go. That identity change is what makes this method stick when apps and spreadsheets don’t.

Start small. Pick three categories this Friday. Withdraw the cash. Fill the envelopes. See how it feels by next Wednesday.

If you can do it for one month, you’ll do it for twelve. And twelve becomes a financial life that doesn’t feel like quicksand anymore.

Save this guide, share it with the friend you always vent about money with, and try one envelope this weekend.

Once you have envelopes running, the next move is protecting yourself from irregular expenses. Our guide to sinking funds for beginners shows exactly how to build that buffer — one small contribution at a time.

Frequently Asked Questions

Q: Does the envelope budgeting method still work in 2026 with everything being digital?

Yes — and arguably better than ever. You can use physical cash for high-leak categories like groceries and dining out, and digital “envelopes” through apps for the rest. The method’s strength isn’t the paper envelope; it’s the predecided spending limit.

Q: How much cash should I keep on hand for the envelope system?

Only what you’ll spend in cash categories that month — usually $300 to $800 depending on your household. Keep most envelopes at home in a secure spot and carry only the one you’ll use that day. Never withdraw a full month of total expenses in cash; bills should stay digital.

Q: What’s the difference between cash stuffing and the envelope budgeting method?

Cash stuffing is essentially the same method with a viral, visual rebrand. The core idea — dividing income into labeled envelopes with set limits — is identical. Cash stuffing just emphasizes the satisfying ritual of physically filling envelopes, which is why it took off on TikTok and Instagram.