Practical, proven strategies to cut your expenses, build savings, and take control of your finances — starting today.

If you’re searching for ways to save money fast, you’re not alone. Between rising grocery bills, sky-high rent, and the constant pull of one-click online shopping, paychecks can feel like they evaporate before the month is half over. The good news? You don’t need a finance degree or a six-figure income to build real savings — you just need the right strategies and the motivation to act on them today.

This guide covers 25 genuinely effective, no-fluff ways to save money fast in the US. These aren’t recycled platitudes from a textbook. They’re practical moves real Americans are making right now to cut costs, reduce debt, and finally get ahead financially. Whether you’re building an emergency fund, paying off a credit card, or simply trying to stop living paycheck to paycheck, something here will work for you.

Why Saving Money Feels So Hard in the US (And How to Change That)

The average American household carries over $10,000 in credit card debt, according to the Federal Reserve’s Consumer Finance Report. Meanwhile, a 2024 Bankrate survey found that nearly 57% of Americans couldn’t cover a $1,000 emergency from savings alone. Those numbers sting — but they also reveal a clear opportunity.

The problem usually isn’t income. It’s the small, invisible spending habits that quietly drain accounts every single month — a forgotten streaming service here, a daily $6 coffee there, a gym membership used twice last January. These aren’t moral failures; they’re just patterns that haven’t been examined yet. And patterns can change.

Section 1: Cut the Obvious (But Ignored) Expenses

1 Audit Every Subscription You’re Paying For

Pull up your last two bank or credit card statements and highlight every recurring charge. You’ll likely find subscriptions you’ve completely forgotten about. A 2024 report by C+R Research found the average American spends $219 per month on subscriptions — nearly double what they estimate they spend.

Common culprits: old streaming services, unused cloud storage, premium app tiers, and forgotten free trials. Cancel anything you haven’t actively used in the last 30 days.

Quick action: Apps like Rocket Money or Trim automatically scan your accounts and flag subscriptions. Most people find $40–$80/month in savings here within minutes.

2 Negotiate Your Bills (More Often Than You Think)

This tip sounds uncomfortable, but it works — and most people never try it. Your cable bill, internet service, and even medical bills are often negotiable. Companies would rather keep you at a lower rate than lose you entirely. A 2023 Consumer Reports survey found 70% of people who negotiated got a discount, averaging $30–$80 per service per year.

Script to use: “Hi, I’ve been a loyal customer for X years, but I’ve found a better deal elsewhere. Is there anything you can do to lower my bill?” Then stop talking. Silence is your ally.

3 Drop Your Cable Bill Entirely

The average American cable bill hit $217 per month in 2024, according to Leichtman Research Group. That’s over $2,600 a year for channels most people scroll past. Replacing cable with one or two streaming services — or Hulu + Live TV and a $30 digital antenna — saves most households $100–$150 every single month.

4 Refinance High-Interest Debt

If you’re carrying credit card balances at 20–28% APR, refinancing to a balance transfer card with a 0% intro APR can save you hundreds annually. The Consumer Financial Protection Bureau estimates the average household with credit card debt pays over $1,500 in interest per year. Balance transfer cards with 12–21 month 0% APR windows (like the Citi Diamond Preferred) are one of the most underused tools in personal finance.

5 Review Your Cell Phone Plan

MVNOs — Mobile Virtual Network Operators like Mint Mobile, Visible, or Consumer Cellular — use the exact same towers as the major carriers but charge a fraction of the price. Solid unlimited plans run $15–$35/month versus the $60–$100+ most people pay. A family of four switching carriers can realistically save $1,200–$2,000 per year with zero drop in coverage quality.

Section 2: Rethink How You Shop

6 Master the Grocery Game

Food is one of the biggest variable expenses in American households — and one of the most controllable. USDA data shows the average American family spends $600–$1,200 per month on food. Here’s what actually moves the needle:

- Shop with a list — impulse purchases account for roughly 60% of unplanned grocery spending

- Buy store brands — made by the same manufacturers 70–80% of the time, at 20–30% less cost

- Check weekly circulars and plan meals around what’s on sale

- Use cashback apps like Ibotta, Fetch Rewards, or Checkout 51

- Buy non-perishables in bulk — Costco and Sam’s Club memberships ($65/year) typically pay for themselves quickly

7 Use the 24-Hour Rule for Non-Essential Purchases

Retailer websites are engineered for impulse buying — countdown timers, “Only 3 left!” banners, one-click checkout. The simple fix: if something costs more than $30 and isn’t a necessity, add it to a list and wait 24 hours. Most people find they no longer want the item after sleeping on it. This single habit saves many Americans hundreds per month without any feeling of deprivation.

8 Buy Used Before Buying New

Facebook Marketplace, OfferUp, ThredUp, Poshmark, and eBay offer furniture, clothing, electronics, and kids’ items at 50–80% below retail price — often in near-perfect condition. A couch retailing for $800 might go for $150 used. A child’s bike priced at $180 new costs $35–$50 secondhand. Over a year of strategic secondhand shopping, a family can save $1,500–$3,000.

9 Stop Paying Full Price for Anything Online

Before completing any online purchase, search “[store name] promo code” in a new tab. Browser extensions like Honey or Capital One Shopping test dozens of coupon codes automatically at checkout.

Bonus trick: Add items to your cart, then abandon it. Many retailers email a 10–15% discount code within 24–48 hours to win you back. This works far more often than people realize.

10 Time Big Purchases Strategically

Knowing when retailers discount specific categories is one of the smartest ways to save money fast on large purchases:

- Mattresses: Memorial Day, Labor Day, Presidents’ Day weekends

- Electronics/TVs: Black Friday, Cyber Monday, post-Christmas

- Cars: End of month, end of quarter, September–November (model year clearance)

- Appliances: February and September

- Clothing: January (winter) and July (summer) end-of-season sales

Section 3: Automate and Optimize Your Finances

11 Automate Your Savings (Pay Yourself First)

This is the most powerful behavioral finance habit that exists. Set up an automatic transfer to savings the day after your paycheck hits — even $50 or $100 at first. Research from the National Bureau of Economic Research found that people who automate savings save an average of 81% more than those who save whatever is left over.

Where to park it: High-yield savings accounts at online banks like Marcus by Goldman Sachs, Ally, or SoFi currently offer 4.5–5% APY versus the 0.01% at traditional banks. On $5,000 saved, that’s $225/year in interest versus $0.50.

12 Build a Zero-Based Budget

Zero-based budgeting (ZBB) assigns every dollar of income a job before the month begins: Income − (expenses + savings + debt payments) = $0. Nothing floats into impulse spending. Apps like YNAB (You Need a Budget) or EveryDollar simplify this process. YNAB reports its users save an average of $600 in their first two months.

13 Use a Cash-Back Credit Card Strategically

If you pay your balance in full every month (non-negotiable — interest wipes out all rewards), a good cash-back card returns 1.5–6% on everyday spending. Top picks for 2025:

- Citi Double Cash: 2% on everything

- Chase Freedom Unlimited: 1.5% base + 3% on dining and drugstores

- Amex Blue Cash Preferred: 6% at US supermarkets (up to $6,000/year), 3% on gas

A household spending $3,000/month on a 2% card earns $720 back annually — for spending they were doing anyway.

14 Refinance Your Mortgage (If the Math Works)

Refinancing makes sense when you can lower your rate by 0.75–1%+, plan to stay 3+ more years, and recoup closing costs within 24–36 months. On a $350,000 mortgage, dropping from 7.5% to 6.5% saves approximately $230/month — nearly $2,800 per year and $14,000 over five years.

15 Eliminate Bank Fees

According to Bankrate’s annual fee survey, the average American pays over $300 in bank fees annually. Online banks like Ally, Chime, and Discover charge zero monthly fees, require no minimum balance, and reimburse ATM fees nationwide. This is a five-minute fix with immediate, permanent results.

Section 4: Slash Everyday Living Costs

16 Cook at Home More (and Meal Prep on Sundays)

The Bureau of Labor Statistics’ 2024 Consumer Expenditure Survey shows the average American spends $3,639 per year dining out. Home-cooked meals cost $2–$5 per serving versus $15–$25 at a restaurant. Shifting from five restaurant meals per week to two, and batch cooking on Sundays, can save a family $300–$600 per month. Meal prepping also cuts food waste — Americans throw away roughly $1,800 in food annually, per USDA estimates.

17 Reduce Your Energy Bill

A few straightforward changes can trim monthly energy costs by $50–$150:

- Install a smart thermostat — the Nest ($130) saves $130–$145/year on average, paying for itself in under 12 months

- Lower your water heater to 120°F (most ship set to 140°F)

- Replace remaining incandescent bulbs with LEDs — 75% less energy, 15–25x longer life

- Seal drafts around windows and doors with weatherstripping (~$20)

- Run dishwashers and washing machines during off-peak utility hours

18 Drive Less, Maintain More

Transportation averages $12,295 per year per household, per BLS data — making it the second-largest expense after housing. Two strategies with outsized impact:

Drive strategically: Combine errands into single trips, carpool when possible, and compare true car ownership costs against rideshare or transit for your actual usage.

Maintain your vehicle: A $40 oil change prevents a $4,000 engine repair. Proper tire inflation improves fuel efficiency by up to 3%, saving $60–$100/year at the pump.

19 DIY Before Hiring Out

YouTube has made dozens of home maintenance tasks genuinely accessible — changing air filters, unclogging drains, patching drywall, replacing outlet covers, installing ceiling fans. Plumbers charge $150–$350 per service hour. A $10 bottle of drain cleaner handles 90% of slow drains. Strategic DIY saves homeowners and renters alike $500–$2,000 per year in service calls.

20 Optimize Your Insurance Premiums

Most people set their insurance once and forget it for years. Every two to three years, shop your policies through a comparison tool like Policygenius or The Zebra. Raising your auto deductible from $500 to $1,000 typically lowers premiums by 15–30%. Bundling home and auto with one insurer saves 10–25% more. The average American overpays $400–$800/year on auto insurance simply from not shopping around.

Section 5: Build Income and Think Long-Term

21 Sell What You Don’t Use

Most American homes contain $1,000–$2,500 in unused or unwanted items, per OfferUp’s 2023 recommerce report. Old electronics, furniture, clothing, sporting equipment, kids’ toys — all have ready buyers. Facebook Marketplace works best for large local items. Poshmark and ThredUp excel for clothing. eBay suits collectibles and electronics. A focused weekend session can put $300–$800 in your account within days.

22 Claim Free Money (Tax Credits and Employer Benefits)

Employer 401(k) match: If your employer matches contributions and you’re not capturing the full match, you’re leaving part of your compensation unclaimed. A 3% match on a $50,000 salary is $1,500/year of free money.

Tax credits: The IRS estimates 20% of eligible taxpayers don’t claim the Earned Income Tax Credit, leaving an average of $2,400 per household unclaimed. Use IRS Free File if your income is under $84,000.

23 Start a Side Hustle (Even a Small One)

Even $200–$400/month in extra income can be transformative — that’s $2,400–$4,800 per year earmarked entirely for savings or debt paydown. Realistic options for 2025–2026:

- Freelancing on Fiverr or Upwork (writing, design, coding, accounting)

- Delivery driving for DoorDash, Instacart, or Amazon Flex on evenings or weekends

- Renting a spare room on Airbnb (hosts average $924/month, per Airbnb’s 2024 data)

- Selling handmade goods or digital products on Etsy

- Local services: lawn care, dog walking, tutoring, house cleaning

24 Leverage the Library (Seriously)

A free library card unlocks: books, e-books and audiobooks via Libby, digital magazines, free video streaming through Kanopy and Hoopla, Rosetta Stone language courses, and LinkedIn Learning. In many cities, library cards also provide free museum and park passes. The average American spends $115/month on entertainment. The library replaces a significant chunk of that at zero cost.

25 Track Your Net Worth Monthly

Tracking net worth is one of the most underrated ways to save money fast — not because it creates money, but because it creates awareness. People who monitor their finances consistently save more and spend less impulsively. Your net worth = total assets (savings, investments, home equity) minus total liabilities (mortgage, loans, credit card balances). Free tools like Empower (formerly Personal Capital) or a simple spreadsheet work perfectly. Schedule 10 minutes on the first of each month.

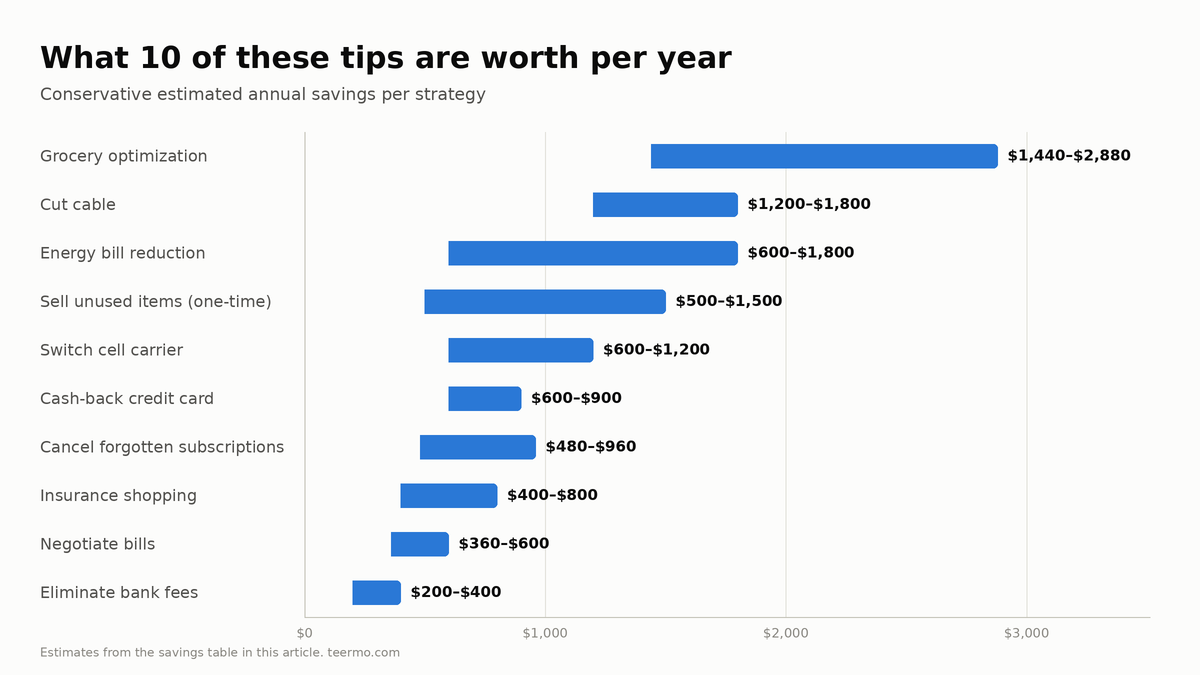

How Much Could You Actually Save?

Here’s a conservative estimate if you implement just 10 of these strategies:

| # | Strategy | Est. Annual Savings |

|---|---|---|

| 1 | Cancel forgotten subscriptions | $480–$960 |

| 2 | Negotiate bills (2 services) | $360–$600 |

| 3 | Cut cable | $1,200–$1,800 |

| 4 | Switch cell carrier | $600–$1,200 |

| 5 | Grocery optimization | $1,440–$2,880 |

| 6 | Cash-back credit card | $600–$900 |

| 7 | Eliminate bank fees | $200–$400 |

| 8 | Energy bill reduction | $600–$1,800 |

| 9 | Insurance shopping | $400–$800 |

| 10 | Sell unused items (one-time) | $500–$1,500 |

| Conservative Total | $6,380–$12,840/year | |

That’s $530–$1,070 per month reclaimed from the exact same income you have today.

Your 7-Day Action Plan

Don’t try to implement everything at once. Here’s a realistic week to build momentum:

Day 1Audit subscriptions and cancel anything unused. Goal: 30 minutes, $40+ in monthly savings identified.

Day 2Call one service provider and negotiate your rate. Goal: 20 minutes, $20–$60/month saved.

Day 3Open a high-yield savings account and set up automatic transfers. Goal: 20 minutes, habit established.

Day 4Check the weekly grocery circular, plan next week’s meals around sales. Goal: 30 minutes, $20–$50 saved on first trip.

Day 5Install Honey or Capital One Shopping. Compare cell plans against MVNO alternatives. Goal: 20 minutes setup.

Day 6List 5–10 unused items on Facebook Marketplace or OfferUp. Goal: 1 hour, $100–$300+ incoming.

Day 7Calculate your net worth. Set a monthly savings goal. Schedule a recurring 10-minute monthly finance check-in. Goal: clarity and momentum.

FAQ: Ways to Save Money Fast in the US

Q1: What are the fastest ways to save money right now with a tight budget?

The fastest ways to save money fast with a tight budget are subscription auditing and bill negotiation — both can yield results within 24 hours without changing your lifestyle. Then automate a small weekly transfer to a high-yield savings account. Even $25/week becomes $1,300 in a year plus interest. Start immediately with whatever amount you can manage.

Q2: How much should I have in an emergency fund?

Financial planners recommend 3–6 months of essential expenses. But if you’re starting from zero, aim for $1,000 first — enough to handle most emergencies (car repair, medical copay, appliance failure) without credit card debt. Build from there incrementally.

Q3: Is a cash-back credit card actually one of the ways to save money fast?

Yes — but only if you pay the full balance every month. Credit card interest (averaging 20%+ APR in 2025) eliminates all rewards instantly if you carry a balance. Used responsibly, a 2% cash-back card on $2,500/month in spending returns $600 per year for purchases you were making anyway.

Q4: What’s the biggest mistake Americans make when trying to save money?

Trying to change too many habits at once, burning out, and quitting. Sustainable savings come from changing two or three things at a time and automating what you can. The second most common mistake is saving “whatever’s left” each month instead of automating a transfer first — that approach almost never works consistently.

Q5: Can I find ways to save money fast without earning more income?

Absolutely. In most cases, the gap between what people earn and what they keep is a spending efficiency problem, not an income problem. Subscription audits, bill negotiation, grocery optimization, and eliminating bank fees alone can recover $300–$600/month from your existing income. Side income accelerates the process, but it’s not required to start making meaningful progress.

Final Thoughts

Finding the right ways to save money fast doesn’t require radical sacrifice or financial expertise. It requires clarity about where your money is actually going, the willingness to make a few strategic changes, and the patience to let those changes compound over time.

Pick five of the 25 strategies above that feel realistic for your situation right now. Master those. Then layer in more. The most expensive financial mistake isn’t a bad investment or an overpaid bill — it’s the decision to keep doing nothing. Your future self will thank you for starting today.