You know that sinking feeling when your car suddenly needs $600 in brake work, your sister’s wedding shows up out of nowhere, and your dog needs a vet visit — all in the same month? That stomach drop is exactly what sinking funds are designed to erase.

Sinking funds beginners often skip this idea because it sounds too simple to actually work. But it’s the closest thing to a cheat code that personal finance has. Instead of getting ambushed by “irregular” expenses (that secretly aren’t irregular at all), you save tiny amounts every month into specific labeled buckets.

In 2026, with cash stuffing trending again and intentional budgeting becoming the default for younger savers, this old-school technique is having a serious comeback. By the time you finish this guide, you’ll know exactly which sinking funds to start, how much to put in each, and how to never get caught off guard by a “surprise” expense again.

What Are Sinking Funds, Really?

A sinking fund is a small savings bucket you build up gradually for a specific, known expense that’s coming later. That’s the whole concept. The name comes from old corporate finance — companies would “sink” small amounts of cash regularly to pay off a big future debt. Same idea, just personal.

Think of it like this: an emergency fund is for things you couldn’t predict (a layoff, a hospital trip). A sinking fund is for things you absolutely could predict but usually pretend you can’t — Christmas, car registration, your annual Costco membership, your kid’s summer camp.

Here’s the thing — Christmas is not an emergency. It happens on December 25th every single year. But for most people, it feels like an emergency every December because they didn’t put $30 a month into a “holiday” envelope starting in January.

That’s the gap sinking funds fill. They turn future-you’s panic into present-you’s quiet little auto-transfer.

→ Related: Simple Budget Plan for Beginners

How Sinking Funds Work (The Simple Math)

The mechanics are almost embarrassingly easy. Take the total amount you’ll need, divide by the number of months until you need it, and save that much every month. That’s it.

Say your car insurance is $900 every six months. Instead of getting hit with $900 in June and panicking, you stash $150 every month into a “Car Insurance” sinking fund. When June rolls around, the money’s just sitting there. No stress, no credit card, no calling your mom.

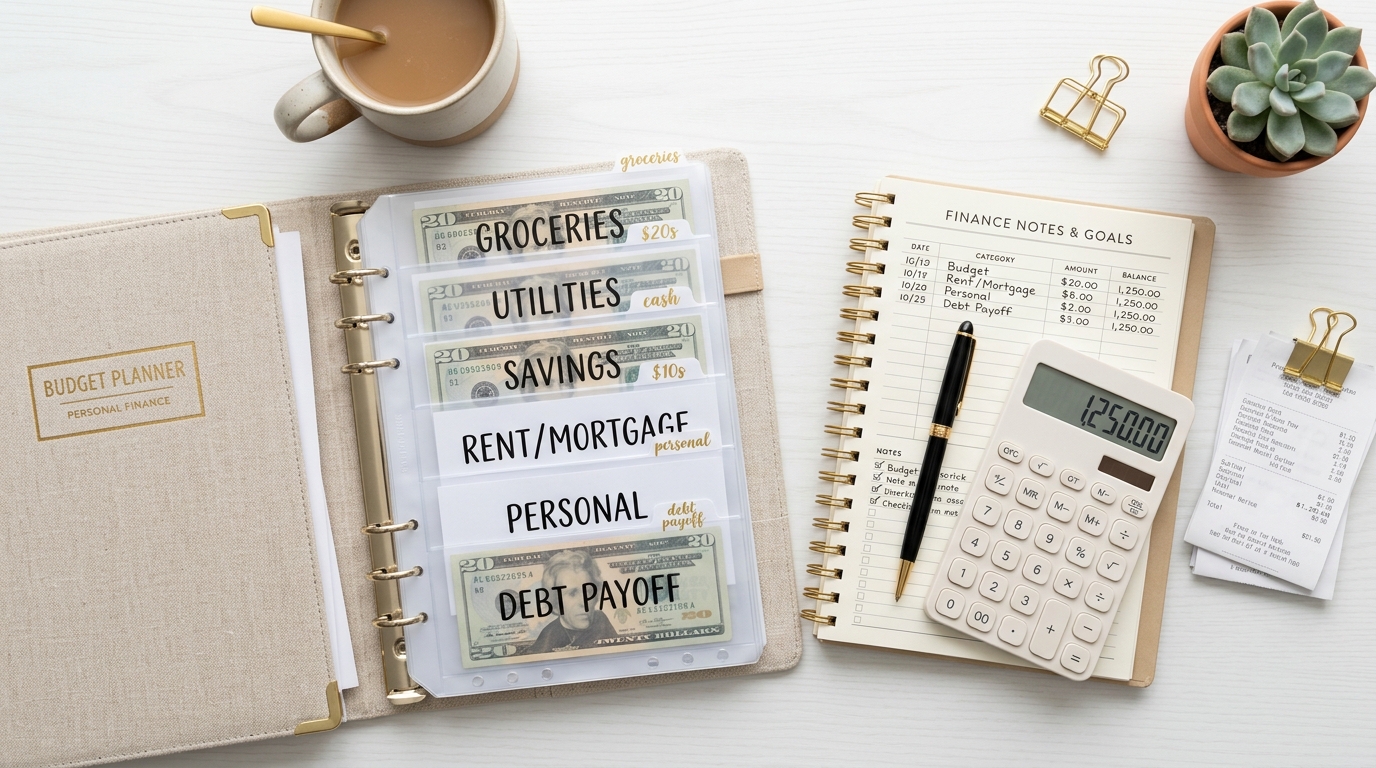

You can do this two ways. Digital sinking funds live in separate high-yield savings accounts or sub-accounts (apps like Ally, SoFi, and Capital One let you create named “buckets”). Physical sinking funds are the cash stuffing version — actual envelopes or a binder with labeled pockets, stuffed weekly or monthly.

The cash stuffing crowd swears the physical version works better because you see and touch your money. Behavioral economists tend to agree — tangible cash creates more friction than tapping a debit card. If you want a full physical system, our budget binder setup guide covers exactly how to build one from scratch.

Why Sinking Funds Beginners Should Care in 2026

Three things are colliding right now that make this the perfect moment to start. First, cash stuffing went mainstream — TikTok and Instagram are full of people pulling out binders and counting twenties. According to a 2025 trend report from NerdWallet, Gen Z and younger millennials are driving a sharp uptick in envelope-style budgeting.

Second, “treat yourself” culture is quietly losing ground to “calm money” culture. People are tired of feeling broke two days after payday. Sinking funds give you the calm version of saving — no deprivation, just preparation. This is the same psychology behind the loud budgeting trend — owning your financial choices instead of hiding from them.

Third, prices on everything from car repairs to weddings have stayed sticky. The buffer you needed in 2020 doesn’t cut it anymore. A working sinking fund system is honestly the cheapest mental health upgrade most beginners can give themselves this year.

If you’ve ever told yourself “I just need to be better with money,” this is the actual mechanism. Not vibes. A system.

7 Sinking Fund Categories Every Beginner Should Start With

You don’t need 20 buckets. Start with the categories that actually catch people off guard. Here are the sinking fund examples I recommend to anyone just starting out.

1. Car Stuff. Repairs, tires, registration, oil changes, insurance premiums. Cars are the #1 budget destroyer for beginners. Even a “reliable” car will cost you something every few months. Save $40–$100/month.

2. Holidays & Gifts. Christmas, Hanukkah, birthdays, anniversaries, Mother’s Day, Father’s Day, Valentine’s. Add them all up — the average US household spends over $900 on Christmas alone. Save $50–$80/month year-round.

3. Medical & Dental. Even with insurance, copays, prescriptions, and that one weird dentist bill will show up. Save $25–$50/month. Bump it higher if you wear glasses or have a chronic condition.

4. Pet Care. Vet visits, vaccines, food, the one emergency you swore wouldn’t happen. Pet owners drastically underestimate this. Save $20–$60/month per pet.

5. Home Maintenance. If you rent, this is renter’s insurance, deposits, moving costs. If you own, it’s HVAC, plumbing, appliances. Save 1% of your home’s value per year, divided by 12.

6. Annual Subscriptions. Amazon Prime, Costco, gym renewals, software, Apple storage. These hit once and feel like ambush charges. Total them up, divide by 12.

7. Fun Money / Travel. Yes, fun is a sinking fund category. Vacations, concerts, weekend trips. Save $50–$200/month based on your goals. This is the bucket that keeps you from raiding the others.

A friend of mine — single mom, two kids, makes about $58k a year — started just these seven funds last January. By December she had a debt-free Christmas for the first time in her adult life. Her line was: “I didn’t make more money. I just stopped getting surprised.”

How to Set Up Your First Sinking Funds (Step-by-Step)

This is the part most guides skip. Here’s the exact order.

Step 1: List your “weird” expenses from last year. Pull up your bank statements and write down every charge over $75 that wasn’t a regular bill. That’s your real sinking fund target list — not what some blog tells you it should be.

Step 2: Total each category and divide by 12. That’s your monthly save amount. Round up to a clean number. If car stuff was $1,400 last year, save $120/month, not $116.67.

Step 3: Pick your method — digital or physical. If you struggle with overspending, go physical (cash stuffing sinking funds 2026 style — labeled envelopes or a zip binder). If you’re disciplined and want interest, open separate sub-accounts in a high-yield savings account.

Step 4: Automate or schedule it. Digital? Set up auto-transfers the day after payday. Physical? Put a recurring reminder on your phone to stuff envelopes the same day each week or month.

Step 5: Start with 3 buckets, not 7. I know — the list above had seven. Don’t do all seven on day one. Pick the three that hurt the most last year. Add the others over the next two or three months as you build the habit.

Step 6: Check in once a month. Not daily. Once. Look at each fund, top it up if you used it, adjust if a category’s running short. Five minutes, max.

A reader emailed me about her first month doing this. She wrote: “I only set up three funds — car, Christmas, and vet. My cat had a UTI in week two. I had $80 already saved. I almost cried. Not because of the cat — because I didn’t have to use my credit card.” That’s the whole feeling sinking funds are selling.

5 Mistakes Beginners Make With Sinking Funds (Don’t Do These)

Most failures aren’t about discipline. They’re about setup errors.

Mistake 1: Too many funds, too fast. People get excited and create 15 categories. By month two they can’t keep up and quit. Start with 3, scale slowly.

Mistake 2: Mixing them all in one account with no labels. If your sinking funds live in the same anonymous “Savings” account as your emergency fund, your brain treats it as one pile and you’ll dip into it. Use named sub-accounts or physical envelopes. Separation is the whole point.

Mistake 3: Underestimating the amount. $20/month for “car stuff” is fantasy. Look at last year’s real spending. Most beginners under-save by 40–60%.

Mistake 4: Using sinking funds as your emergency fund. They are not the same thing. If you raid your Christmas envelope for a hospital bill, Christmas still arrives in December. Build a small starter emergency fund first ($500–$1,000), then layer sinking funds on top.

Mistake 5: Quitting after one bad month. You will skip a month. Your car will eat the whole fund and then need more. That’s not failure — that’s the system catching what would’ve otherwise been credit card debt. Restart the next paycheck.

Final Thoughts

Remember that car-brakes-wedding-vet month from the intro? With even three sinking funds running, that month becomes annoying instead of catastrophic. The bills still come — you just already have the money waiting.

That’s the real shift sinking funds offer beginners. It’s not about saving more. It’s about saving on purpose, in advance, in named buckets, so future-you isn’t constantly bailing out past-you. Whether you go full cash stuffing with a binder of envelopes or you click “create new sub-account” in your banking app, the mechanism is the same: tiny amounts, specific labels, consistent timing.

Pick three categories tonight. Total last year’s spending in each. Divide by 12. Move that much by Friday — physically, digitally, doesn’t matter. You will feel the difference within one paycheck.

If you want to go deeper, the next step is layering sinking funds on top of a real monthly budget. Check out our cash stuffing for beginners guide or the full budget binder setup walkthrough to build your physical system today.

Frequently Asked Questions

Q: What’s the difference between a sinking fund and an emergency fund?

An emergency fund is for unpredictable events — job loss, medical emergencies, urgent home damage. A sinking fund is for predictable future expenses like Christmas, car registration, or annual insurance. Sinking funds beginners often confuse the two and end up draining one for the other, which defeats the whole purpose. Keep them in separate accounts or envelopes.

Q: How many sinking funds should a beginner have?

Start with three. The most common beginner sinking funds are car expenses, holidays/gifts, and one personal category like pet care or travel. Once you’ve kept those funded consistently for two or three months, add more. Trying to launch ten buckets on day one is the fastest way to give up by month two.

Q: Is cash stuffing or digital sinking funds better in 2026?

Both work — it depends on your personality. Cash stuffing creates physical friction that helps overspenders, which is why it’s so popular right now. Digital sub-accounts earn interest and run on autopilot, which suits people who already have decent self-control. Many beginners do a hybrid: cash for “fun” and “gifts,” digital for “insurance” and “car.”

→ Related: How to Live on $1,500 a Month: 7 Real Steps for 2026