You stare at your bank app. The number is small. Or zero. Or negative. And every “budgeting tip” online seems to assume you already have a paycheck, an emergency fund, and a spreadsheet habit.

That gap between advice and reality is exactly why most people give up before they begin.

Here’s the truth nobody says out loud: learning how to start a budget with no money isn’t about money at all — at least not in the first week. It’s about getting your eyes back on what’s actually happening so the panic stops running the show.

With rent, groceries, and basic bills hitting harder in 2026 than at any point in the last decade, more Americans are starting from scratch than ever. Students, gig workers, the recently laid-off, the chronically underpaid — all in the same boat.

This guide is built for that boat. No shaming, no “just cut out lattes,” no pretending you have $500 to invest. Just a calm, step-by-step plan to take back control when your starting line is zero.

By the end, you’ll have a working budget, a survival plan, and — maybe for the first time in a long time — a small, quiet feeling that says: okay, I can do this.

Why Learning How to Start a Budget With No Money Matters Right Now

A budget isn’t a punishment. It’s a flashlight in a dark room.

When you have very little, every dollar carries weight. One missed bill snowballs into late fees, overdrafts, and that awful stomach-drop feeling when you open your mailbox. Budgeting when you’re broke isn’t optional — it’s the single fastest way to stop bleeding money you don’t have.

That mismatch is why “money management basics 2026” is one of the fastest-growing search topics this year. People aren’t trying to get rich. They’re trying to stop drowning.

And here’s the thing — you don’t need income to start. You need awareness. The shift from “I have no idea where my money goes” to “I know exactly what’s coming in and going out” is the entire first stage of getting out. A simple budget plan doesn’t require a big paycheck — it requires a clear picture.

Step 1: Face the Numbers Without Flinching (The 10-Minute Money Mirror)

Before any spreadsheet, do this: sit down and list everything. Every account balance. Every debt. Every recurring charge — even the $4 one you forgot about. Even if it’s all zero.

This is the part most people skip because it hurts. Do it anyway.

Take ten minutes. Open your bank app, your wallet, any unpaid bills on the counter. Write it all on one page or one notes app screen. No judgment. No math yet. Just the picture.

I know a college student in Ohio who did exactly this last winter. She had $11 to her name and three overdue bills. She cried, then she made the list. Two months later she wasn’t rich — but she’d stopped the bleeding and built an $80 cushion. That cushion only existed because she looked.

The reason facing the numbers works is biological: anxiety thrives on the unknown. The moment you can see the full shape of your situation, your brain stops simulating worst-case scenarios on a loop. That alone is worth the discomfort.

Step 2: Separate “Survival” From “Everything Else”

Now divide your expenses into two buckets — and only two:

- Survival: rent or shelter, basic food, utilities you can’t lose (electricity, water, phone if you need it for work), transportation to job interviews or work, essential medication

- Everything else: streaming services, takeout, clothing beyond basics, subscriptions, “small” daily spending

This is the foundation of any emergency budget plan. When income is zero or near zero, survival items get protected first. Everything else gets paused, downgraded, or canceled — not forever, just for now.

Be honest. Internet probably belongs in survival in 2026. A $15 streaming bundle does not.

A useful gut-check: if this expense disappeared tomorrow, would my life get measurably worse, or just slightly less fun? Survival items pass the first test. Comfort items only pass the second.

Step 3: Find Hidden Money You Didn’t Know You Had

Budgeting on zero income sounds impossible until you realize most people already have small money leaks they can plug — even when broke.

Check these in order:

- Subscriptions — Cancel anything auto-billing you that you used less than twice last month. Free trials you forgot about. Old gym memberships. The average American leaks $200+ a year on these.

- Bank fees — Call your bank and ask, politely, if they’ll waive maintenance or overdraft fees. They often will, especially if you’ve never asked before. This is free money.

- Unused gift cards or store credit — Check your email for old promo balances. People genuinely forget about $20–$50 sitting in app wallets.

- Returnable items — Anything within return windows? Bring it back. Cash today beats clutter tomorrow.

- Spare change and bottle deposits — Sounds small. In a survival budget, $7 is groceries for a day.

These aren’t life-changing amounts individually, but stacked together they often produce the first $30–$100 a beginner budget needs to function.

Step 4: Track Every Dollar for 7 Days (Yes, Even the $1 Ones)

For one week, write down every single thing you spend money on. Coffee. Bus fare. A bag of chips. All of it.

This sounds tedious. It is. It also works faster than any app.

The reason is simple: tracking changes behavior. The act of recording a purchase forces a half-second pause where you ask, do I actually want this? Studies in behavioral economics consistently show that just tracking spending — without changing anything else — reduces it by 10–20% on average.

I know what you’re thinking — I don’t have money to track, so what’s the point? The point is that even tiny purchases reveal patterns. Maybe you’ve been spending $4 a day at the corner store. That’s $120 a month you didn’t know was leaving. In a broke budget, $120 is a phone bill.

Use a free notes app. A scrap of paper. A note on your phone’s lock screen. The tool doesn’t matter. Consistency does. If you want a physical system, a simple budget binder with a tracking page costs about $5 and works better than most apps.

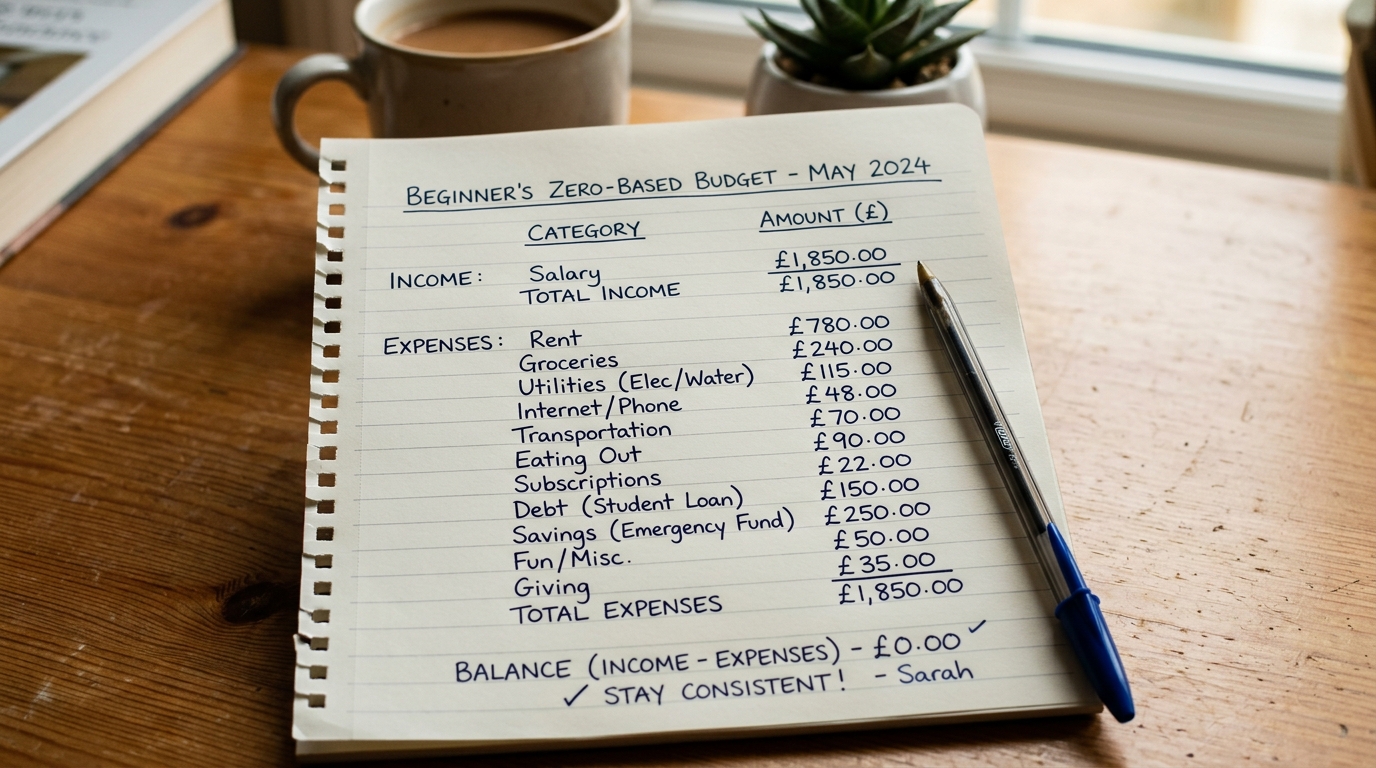

Step 5: Build a Bare-Bones “Zero-Based” Budget

This is the heart of how to start a budget with no money — and it’s simpler than it sounds.

A zero-based budget means: every dollar you do get (even $20 from a side gig) gets a job before it arrives. Income minus expenses should equal zero on paper, because every dollar is assigned somewhere.

Here’s a starter template for someone bringing in $0–$500 a month:

- Shelter/utilities: whatever’s required

- Food: $40–$60 per week (rice, beans, eggs, frozen vegetables, peanut butter — boring works)

- Transportation: only what’s essential

- Emergency cushion: $5–$20 (yes, even when broke — momentum matters)

- One small joy: $5 a week for something that keeps you human (coffee, library late fee, cheap snack)

That last category surprises people. Leaving room for one small joy is what separates a budget you’ll actually follow from one you’ll abandon in three days. Total deprivation backfires every time.

Step 6: Open the Right (Free) Accounts and Tools

You don’t need a financial advisor. You need three things, and all are free:

- A checking account with no minimum balance and no monthly fee. Online banks like Chime, Ally, Discover, or Capital One 360 work well for beginners. Avoid traditional banks that charge $12/month if your balance dips below $1,500.

- A separate savings account — even if it starts with $1. The act of having a “savings” label trains your brain to protect it differently than checking money.

- One free budgeting tool. A notebook is fine. So is a Google Sheet. If you want an app, free tiers of EveryDollar, Goodbudget, or even a YNAB trial work. You can also use the cash stuffing envelope method — no app required, just labeled envelopes and physical cash.

Don’t overbuild your toolkit before you have habits. Beginner budgeting with low income fails most often when people spend more time researching apps than tracking expenses.

Step 7: Stack Tiny Wins Until They Become Income

The final step in any emergency budget plan: turn the budget into a launchpad, not a cage.

Once you’ve got a week of tracking, a cushion of even $10, and your survival expenses locked, look outward. Quick income ideas that don’t require startup money:

- Sell unused items (clothes, electronics, books) on Facebook Marketplace, Mercari, or Poshmark

- Sign up for paid plasma donation if eligible — $50–$100 a week in many US states

- Take on micro-tasks via apps like UserTesting, Prolific, or Field Agent ($5–$30 per task)

- Offer one neighborhood service: dog walking, lawn mowing, snow shoveling, tutoring

- Apply to gig work that pays weekly (DoorDash, Uber, Instacart) if you have the means to start

The goal isn’t to get rich — it’s to add even $40 a week to a budget that previously had nothing. Forty dollars a week becomes $160 a month. That’s gas. Or groceries. Or the start of a real sinking fund for car repairs, medical costs, or the next irregular bill that blindsides you.

Tiny wins compound. That’s the whole secret.

5 Common Mistakes Beginners Make (And How to Avoid Them)

Mistake 1: Trying to be perfect on day one. A messy budget you actually use beats a perfect spreadsheet you abandon. Start ugly. Improve later.

Mistake 2: Cutting all joy. Going from comfort spending to monk-mode lasts about four days. Build in one tiny pleasure. It’s not a luxury — it’s a sustainability tool.

Mistake 3: Comparing yourself to TikTok finance influencers. Most are selling something. Their “I saved $30k in a year” budget assumes a $90k salary. You’re not behind. You’re starting where you are.

Mistake 4: Skipping the cushion because it’s “too small to matter.” A $20 cushion has stopped more financial spirals than any investment strategy. It’s not about the amount — it’s about not falling back to zero. This is the same logic behind sinking funds — small, consistent saving prevents big emergencies.

Mistake 5: Not telling anyone. Quiet shame keeps you stuck. Telling one trusted person — a friend, partner, parent, even an online community — adds accountability and often surfaces help you didn’t know was available. The loud budgeting movement is built on exactly this idea: saying your financial truth out loud removes the shame and adds social support.

Final Thoughts: You’re Not Behind — You’re Starting

Remember that bank app screen from the beginning? The one that made your chest tight?

It’s still there. But now you have a flashlight. You know what’s on it, what to protect, what to cut, and what the next small move looks like. That’s not a small shift — that’s the entire difference between drowning and treading water.

Learning how to start a budget with no money isn’t about scarcity. It’s about reclaiming attention. When you watch your dollars closely, even the few you have, they start working harder. Opportunities you couldn’t see before become visible. The panic dial turns down.

You don’t need to do all seven steps today. Pick one. Maybe it’s the 10-minute money mirror. Maybe it’s canceling that one subscription. Maybe it’s just writing down what you spent yesterday.

Save this post. Come back tomorrow and do step two. That’s how every budget — and every recovery — actually gets built.

Once your basics are locked, the next move is protecting future-you from surprise expenses. Our guide to sinking funds for beginners shows exactly how to do that — no big income required.

Frequently Asked Questions

Q: Can you really start budgeting with no income at all?

Yes. The first phase of budgeting isn’t about allocating income — it’s about mapping what you owe, what you spend, and what you have. Even with zero coming in, tracking outflow and reducing leaks (subscriptions, fees, impulse spending) creates immediate savings. Income comes next, but awareness comes first.

Q: How much money do I need to start a budget?

Zero. A budget is a plan, not a balance. You can build one with a pen and the back of an envelope. The misconception that budgeting requires apps, software, or a minimum savings amount is exactly why most people never start. Begin with what you have today — even if that’s just $3 and a notebook.

Q: What’s the easiest budgeting method when you’re broke?

The zero-based bare-bones budget covered in step 5. You give every dollar a job — even tiny amounts — and prioritize survival expenses first. It works because it’s brutally simple, requires no software, and forces honest decisions without the overwhelm of complex percentage-based systems like the 50/30/20 rule, which assumes a reliable income most broke beginners don’t have yet.