Building a Budget on a $50K Salary Is More Doable Than You Think

If you’ve been trying to figure out how to create a budget on a 50K salary in the US, you’re in the right place. A $50,000 annual income sounds solid until you see your first paycheck — after taxes, health insurance, and maybe a 401(k) contribution, your take-home pay can feel surprisingly thin. If you’ve ever stared at your bank account on the 28th of the month wondering where it all went, you’re definitely not alone.

Here’s the truth: a 50K salary in the US is right around the median income for a single earner in many mid-sized cities. It’s not lavish, but it’s absolutely workable — as long as you have a monthly budget plan in place. And that’s exactly what this guide is here to help you build.

Whether you’re fresh out of college, switching careers, or simply trying to get your money in order, creating a monthly budget is the single most powerful step you can take for your financial health. No special apps required, no finance degree needed. All you need is a clear picture of what’s coming in, what’s going out, and a few smart choices along the way.

So, let’s dig in.

What Does a $50K Salary Actually Look Like After Taxes?

Before you can set up a budget on a 50K salary in the US, you first need to know your real starting number — your take-home pay.

A $50,000 gross salary works out to roughly $4,167 per month before any deductions. However, here’s what happens after the government takes its share (assuming you’re single with a standard deduction — you can verify your own withholding using the IRS Tax Withholding Estimator):

- Federal income tax: ~$4,500/year (~$375/month)

- Social Security (6.2%): ~$3,100/year (~$258/month)

- Medicare (1.45%): ~$725/year (~$60/month)

As a result, you’re left with approximately $3,474/month in take-home pay — and that’s before your state’s income tax. For example, in states like Texas or Florida where there’s no income tax, you keep more. In contrast, if you live in California or New York, you’ll need to deduct another $150–$300/month.

For this guide, we’ll work with a $3,200/month take-home figure — a practical, realistic number that accounts for state taxes and common pre-tax deductions like a basic health insurance premium. Feel free to adjust up or down based on your specific situation.

Step 1: Track Every Dollar for 30 Days Before You Budget

Here’s something most budgeting guides skip entirely: before you build a monthly budget on a 50K salary, spend one full month just tracking your spending. Don’t change anything yet. Simply observe.

To do this, use your bank’s transaction history or a free app like Mint or YNAB’s free trial. Categorize everything — groceries, dining out, subscriptions, gas, whatever comes up. At the end of those 30 days, you’ll have something truly valuable: data about your actual life, not some idealized version of it.

Most people discover two or three spending categories they didn’t realize were quietly eating their budget alive. Some of the most common culprits include:

- Streaming subscriptions (the average American pays for 4–5 services they rarely use)

- Dining out more often than they remember

- “Convenience” purchases — delivery fees, vending machines, impulse buys

- Forgotten recurring charges (gym memberships, software trials that auto-converted)

In short, this 30-day audit is the foundation your entire budget on a 50K salary will be built on. Skip it and you’re guessing. Do it and you’re planning with purpose.

Step 2: Choose a Budget Framework That Fits Your 50K Salary

There’s no single “right” way to build a budget on a 50K salary in the US. Instead, the best system is simply the one you’ll actually stick with. Here are three popular frameworks, each with genuine merit:

The 50/30/20 Rule — A Great Starting Point for a 50K Salary Budget

This is the most widely recommended starting framework — and for good reason. It’s simple, flexible, and works well for most people earning around $50K a year.

- 50% to Needs: Rent, utilities, groceries, transportation, minimum debt payments

- 30% to Wants: Dining out, entertainment, travel, hobbies

- 20% to Savings & Debt Paydown: Emergency fund, retirement, extra debt payments

So, on a $3,200/month take-home, that breaks down like this:

- Needs: $1,600

- Wants: $960

- Savings/Debt: $640

This is a great starting point. However, if you live in a high-cost city like San Francisco, Boston, or Seattle, your “needs” bucket will likely push well past 50%. That’s okay — simply adjust the framework to match your reality, not the other way around.

Zero-Based Budgeting

With this method, every dollar gets a job. You assign each dollar of your income to a specific category until you reach zero — not because you’ve spent everything, but because you’ve planned everything, including savings.

This approach requires more effort upfront. Nevertheless, it tends to produce the best results for people who’ve struggled with overspending in the past. Because every category has a set number, you can’t easily ignore where your money is going.

The Pay-Yourself-First Method

With this approach, before you pay any bills, you transfer your savings amount into a separate account automatically. Then you simply live on what’s left. This method is especially powerful for anyone who finds that “I’ll save whatever’s left over” consistently results in saving nothing.

For a 50K salary in the US, automating even $200–$300/month into savings before you touch your paycheck can build meaningful financial security over time.

Step 3: Map Out Your Actual Monthly Budget on a 50K Salary

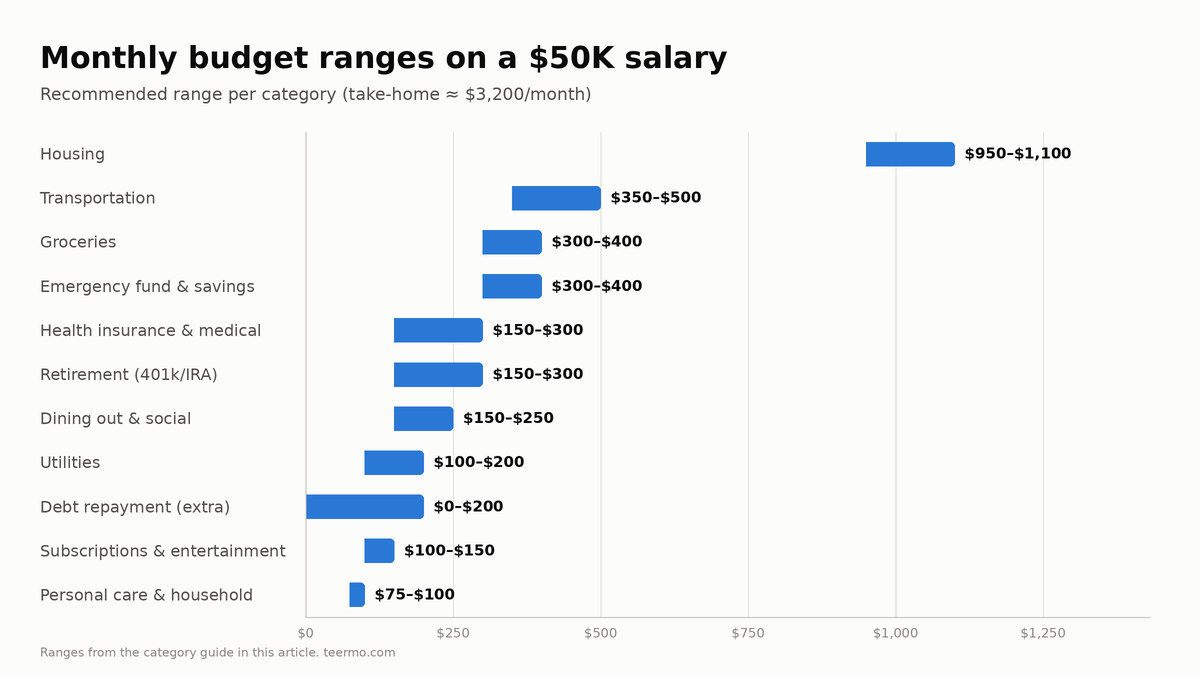

Here’s a detailed, realistic monthly budget for someone earning $50K a year with $3,200/month in take-home pay. This is built for a single person living alone in a mid-cost city — think Charlotte, NC; Columbus, OH; Austin, TX; or Denver, CO — rather than an expensive metro like NYC or San Francisco.

Housing: $950–$1,100

Rent is typically your biggest monthly expense. Because of this, it deserves the most attention. Financial advisors generally recommend keeping housing at or below 30% of your gross income — that’s about $1,250/month for a $50K earner. For take-home budgeting purposes, aim for 30–35% of your net pay, which puts you in the $960–$1,120 range.

If your rent is higher than that, look for ways to offset the cost — for instance, bringing in a roommate, downsizing to a smaller unit, or relocating to a slightly more affordable neighborhood.

Sample allocation: $1,000

Transportation: $350–$500

This category includes your car payment (if you have one), insurance, gas, and maintenance — or public transit costs if you don’t own a car. AAA’s annual “Your Driving Costs” study estimates the average annual cost of owning and operating a vehicle was around $12,000 in 2024, which works out to $1,000/month. That’s clearly too high when you’re building a budget on a 50K salary.

Therefore, if you own a car, aim for a modest, paid-off or low-payment vehicle. As a good rule of thumb, keep total transportation costs at or below 15% of your take-home pay.

Here’s a rough breakdown:

- Car insurance: ~$120–$150/month

- Gas: ~$100–$150/month, depending on your commute

- Car payment (if applicable): Aim for under $200/month

- Maintenance reserve: ~$50/month

Sample allocation: $400

Groceries: $300–$400

According to the USDA’s official food cost reports, a single adult on a moderate-cost plan should expect to spend around $350–$400/month on groceries as of 2024. You can spend less with meal planning and fewer impulse purchases — or more if you have specific dietary needs or strong preferences.

To keep costs down, consider these habits:

- Meal prep 2–3 times a week to cut food waste

- Choose store brands for everyday staples (the quality difference is rarely worth the extra cost)

- Always shop with a list, and eat before you go — it really does help

Sample allocation: $350

Utilities: $100–$200

This covers electricity, gas or heat, water, and trash. According to the U.S. Energy Information Administration, the average American household spends about $160/month on utilities. Additionally, internet service adds another $50–$80/month on top of that.

Sample allocation: $175 (utilities + internet)

Health Insurance & Medical: $150–$300

If you have employer-sponsored insurance, your premium is likely deducted pre-tax from your paycheck — which means it’s already not counted in your $3,200 take-home figure. Even so, out-of-pocket costs like copays, prescriptions, and dental care can still add up quickly.

As a result, it’s smart to budget a monthly reserve for medical expenses, even if you’re generally healthy. Unexpected costs have a way of appearing at the worst times.

Sample allocation: $150

Personal Care & Household Supplies: $75–$100

This includes toiletries, cleaning products, haircuts, and similar everyday items. It’s easy to underestimate this category. Fortunately, your 30-day spending audit will give you a precise number to work with.

Sample allocation: $80

Subscriptions & Entertainment: $100–$150

Be honest with yourself here. List every subscription you pay for and ask: did I actually use this last month? If not, cancel it. The average American spends far more on subscriptions than they realize — often over $200/month without tracking it.

Instead of letting subscriptions pile up, keep this category intentional. One or two streaming services, a music app, perhaps a gym membership. Not all of them simultaneously.

Sample allocation: $120

Dining Out & Social: $150–$250

This is separate from your grocery budget. It covers restaurant meals, coffee runs, happy hours, and birthday dinners. On a 50K salary budget, even small changes in this area can make a noticeable difference in your monthly balance.

That said, don’t cut it to zero. Eliminating social spending entirely is a fast route to budget burnout — and then abandoning the budget altogether.

Sample allocation: $200

Emergency Fund & Savings: $300–$400

This line item is non-negotiable. If you don’t yet have at least 3 months of expenses saved, building your emergency fund should be your top priority — even before paying extra on debt or investing.

Your target is 3–6 months of essential expenses, which works out to roughly $6,000–$10,000 for this budget profile. At $300/month, you’d reach $3,600 in a year — a solid, meaningful cushion.

Sample allocation: $300

Retirement (401k / IRA): $150–$300

If your employer offers a 401(k) match, contribute at minimum enough to capture the full match. That is genuinely free money — an immediate 50–100% return on that portion of your savings. No other investment comes close to matching that.

If you don’t have a 401(k) available, open a Roth IRA instead. The IRS sets the contribution limit at $7,000/year for 2025. Even a $150/month contribution gets you $1,800/year — a meaningful start toward long-term security.

Sample allocation: $200

Debt Repayment (Beyond Minimums): $0–$200

If you carry student loans, credit card balances, or a personal loan, this category matters a great deal. Paying more than the minimum each month shortens your payoff timeline and saves you real money in interest over time. As a general rule, always prioritize your highest-interest debt first.

Sample allocation: $125 (if applicable)

The Full Monthly Budget Snapshot for a 50K Salary

| Category | Monthly Amount |

|---|---|

| Rent/Housing | $1,000 |

| Transportation | $400 |

| Groceries | $350 |

| Utilities + Internet | $175 |

| Health/Medical | $150 |

| Personal Care & Household | $80 |

| Subscriptions & Entertainment | $120 |

| Dining Out & Social | $200 |

| Emergency Fund | $300 |

| Retirement (IRA/401k) | $200 |

| Debt Repayment | $125 |

| Miscellaneous / Buffer | $100 |

| Total | $3,200 |

Notice the “Miscellaneous / Buffer” line at the end. This isn’t a slush fund — it’s simply an acknowledgment that real life doesn’t fit neatly into spreadsheets. Car registration is due once a year. A friend gets married and you need a gift. Your laptop dies unexpectedly. Because of this, having a small buffer prevents one surprise expense from throwing off your entire budget on a 50K salary.

Step 4: Use Sinking Funds to Stay Ahead of Big Expenses

One of the most underrated tools in any monthly budget — especially when you’re managing a 50K salary in the US — is the sinking fund: a dedicated savings account set aside for a known future expense.

Here’s how it works: identify expenses you know are coming, but that don’t happen every month. Common examples include:

- Car registration: ~$100–$200/year

- Annual subscriptions (such as Amazon Prime or antivirus software): ~$150–$200/year

- Holiday gifts: $300–$600/year

- Vacations: $1,000–$2,000/year

- Car maintenance: ~$600/year

After you’ve listed them, add those amounts up, divide by 12, and set that monthly amount aside in a separate savings account. Then, when the expense arrives, the money is already there waiting. No scrambling, no credit card debt.

For example, if you want a $1,200 vacation and plan to spend $400 on holiday gifts, that’s $1,600/year — or $133/month into a sinking fund. Because you’ve saved consistently, by December the money is ready and waiting.

Step 5: Deal With the Tough Realities of Budgeting on a 50K Salary

What If Rent Is Too High for This Budget?

In many US cities, $1,000/month for rent simply isn’t realistic. If you’re in Chicago, Denver, or a similar metro area, a one-bedroom apartment can easily run $1,400–$1,700/month. That, in turn, takes up a much larger share of your $3,200 take-home.

If housing costs more than your 50K salary budget allows, something else has to be reduced. Here are some practical options:

- Get a roommate, which can cut housing costs by 30–50%

- Reduce dining out more aggressively

- Pause the vacation sinking fund temporarily

- Consider adding a side income (more on this in the next section)

Remember, the 50/30/20 rule isn’t a law — it’s simply a guideline. What truly matters is that the numbers balance at the end of the month.

What About Student Loans?

According to Federal Student Aid, the average monthly federal student loan payment is around $300–$400 for borrowers on a standard 10-year repayment plan. That’s a significant chunk of a 50K salary budget, so it’s worth planning for carefully.

If payments feel unmanageable, Income-Driven Repayment (IDR) plans can lower your monthly amount based on your income. It’s worth calling your loan servicer to explore the options available to you.

What If You’re Paying Off Credit Card Debt?

Credit card debt is expensive. According to the Federal Reserve’s Consumer Credit data, the average credit card APR hovered around 21–22% in 2024. Because of that high cost, paying it off should feel urgent when you’re working with a budget on a 50K salary.

When it comes to strategy, you have two main choices. The avalanche method — paying the highest-interest debt first — saves the most money overall. On the other hand, the snowball method — paying the smallest balance first — provides motivating early wins that help some people stay on track. Either approach, however, beats making only the minimum payment, which can stretch a debt out for a decade or more.

Step 6: Grow Your Income Beyond Your 50K Salary

A budget only addresses one side of the financial picture. The other side is income — and a 50K salary in the US doesn’t have to be your permanent ceiling.

Ask for a Raise

If you’ve been in your role for more than a year and have clear results to point to, a raise conversation is absolutely worth having. For instance, a 5–10% increase bumps your annual salary to $52,500–$55,000, which adds $150–$400/month to your take-home pay. Over time, that difference adds up significantly.

Before the conversation, research your market rate using the Bureau of Labor Statistics Occupational Employment Statistics tool or sites like Glassdoor and LinkedIn Salary. That way, you’ll have solid data to back up your ask.

Develop a Side Income

In 2024, roughly 36% of Americans had some form of side income, according to Bankrate. The options are wide-ranging, so there’s likely something that fits your skills and schedule:

- Freelancing in your professional field

- Driving for a rideshare service

- Selling items online through eBay, Facebook Marketplace, or Etsy

- Tutoring or teaching a skill you already have

- Renting a spare room or even a parking space

Even an extra $300–$500/month, when directed toward savings or debt paydown, can meaningfully speed up your financial progress on a 50K salary budget.

Consider Skills That Pay More

Not every income boost has to come from a raise or side hustle. Certifications, continuing education, and well-timed job changes can also move the needle significantly. For example, moving from $50K to $60K adds roughly $450/month to your take-home — more than any single budget tweak for a 50K salary can realistically accomplish.

Step 7: Build Money Habits That Make Your 50K Salary Budget Stick

A budget is a document. Financial stability, though, is a habit. Here’s what separates people who budget successfully from those who set one up in January and quietly abandon it by March:

Weekly money check-ins. Set aside 10–15 minutes every Sunday to review what you spent that week. This isn’t about judging yourself — it’s about staying aware. For example, if you’ve already spent $180 on dining out and it’s only the 20th, catching that drift early lets you adjust before the month ends.

Automate what you can. Set up automatic transfers to your savings account on payday. Similarly, automate your retirement contributions. The less you rely on willpower, the more consistent your results will be.

Review your budget quarterly. Life changes — and so should your budget. A raise, a move, a new car, or a relationship change can all shift your financial picture. Therefore, a quarterly budget review ensures your plan stays current and relevant.

Give yourself a “fun fund.” Sustainable budgets don’t feel like punishment. Budget a specific, guilt-free amount for fun spending each month. When it’s gone, it’s gone — but while you have it, enjoy it freely and without guilt.

Common Mistakes to Avoid When Budgeting on a 50K Salary

Budgeting based on gross income instead of take-home pay. Always base your budget on your actual bank balance, not your salary before deductions.

Forgetting irregular expenses. Annual fees, car registration, medical deductibles — these feel like surprises, but they’re actually predictable. As mentioned earlier, sinking funds solve this problem completely.

Setting targets that are too strict. If you currently spend $400/month dining out, cutting to $50 overnight will almost certainly fail. Instead, try $300 first and work down from there.

Investing before having an emergency fund. An emergency fund isn’t an investment — it’s insurance. Without it, even one car repair can push you into credit card debt and erase your financial progress.

Comparing your budget to others. Your coworker’s financial situation, family support, debt load, and cost of living may be completely different from yours. Budget for your own life, not someone else’s.

Real-Life Example: How Maria Runs Her 50K Salary Budget

Maria is 28 and lives in Columbus, Ohio. She works as a marketing coordinator and earns $50,000/year. After taxes and her employer’s health insurance premium, her take-home is about $3,100/month.

Her rent is $875 for a one-bedroom apartment. She drives a paid-off 2019 Honda Civic, pays about $1,200/year in car insurance, and has modest gas costs. She also carries $18,000 in student loans at 5.5% interest.

Here’s how her actual monthly budget on a 50K salary looks:

- Rent: $875

- Car insurance + gas: $230

- Groceries: $280

- Utilities + internet: $160

- Health (copays, prescriptions): $80

- Subscriptions (Netflix, Spotify, gym): $90

- Dining out: $175

- Student loans (standard repayment): $190

- Emergency fund: $250

- Roth IRA: $150

- Miscellaneous / buffer: $120

- Total: $2,600

As a result, Maria has $500/month left over, which she splits between a vacation sinking fund ($150), extra student loan payments ($200), and additional savings ($150).

She’s not wealthy by any stretch. However, she has a plan — and 14 months in, her emergency fund has grown to $4,200, her student loan balance is shrinking faster than the standard schedule, and she just returned from a long weekend in Nashville she’d been saving for since January.

That’s what a working budget on a 50K salary actually looks like in practice.

FAQ: Budget on a 50K Salary in the US

Q: Is a $50K salary enough to live comfortably in the US?

A: It depends heavily on where you live and what your lifestyle looks like. In many mid-sized cities — such as Columbus, Indianapolis, Charlotte, or San Antonio — a budget on a 50K salary in the US can absolutely support a comfortable life, with room for savings and some fun spending. In high-cost metros like New York City, San Francisco, or Boston, however, $50K is significantly more of a stretch. The key, in either case, is aligning your spending with your actual take-home pay rather than your gross salary, and being intentional about housing costs — which typically make or break this budget.

Q: How much should I save each month on a $50,000 salary?

A: A reasonable target is 15–20% of your take-home pay. On a $3,200 net income, that works out to roughly $480–$640/month. This should include both emergency savings and retirement contributions. If you’re starting from zero, prioritize building a $1,000 starter emergency fund first. Then tackle any high-interest debt. After that, work toward 3–6 months of expenses in savings while also contributing to retirement accounts. If 20% feels out of reach right now, simply start with whatever amount you can automate — even $100/month builds the habit and adds up over time.

Q: What’s the best budgeting method for a 50K salary in the US?

A: For most people who are new to building a budget on a 50K salary, the 50/30/20 rule is the best place to start because it’s flexible and easy to follow. However, if you have significant debt or you’ve struggled to save consistently in the past, zero-based budgeting — where every dollar has a specific purpose — tends to deliver better short-term results. Ultimately, the “best” method is the one you’ll actually use on a regular basis. Try one for two months; if it’s not working, switch. Also, don’t confuse having a budgeting app with having a budgeting habit — the tool matters far less than the weekly practice.

Q: How do I budget if my income is irregular or I get paid bi-weekly?

A: If you’re paid bi-weekly, you receive 26 paychecks per year. That means two months of the year will have three paycheck deposits instead of two. The smartest approach is to build your 50K salary budget around two paychecks and treat those third-paycheck months as a bonus — sending the extra money directly to savings or debt paydown. For truly irregular income, such as freelance or commission-based work, always budget based on your lowest recent month, not your average. Then, any amount above that floor goes to savings first, so you can draw from it during slower months.

Q: Should I pay off debt or save first on a $50K salary?

A: Both — but in a specific order. First, build a small emergency fund of $1,000, so that one unexpected expense doesn’t push you deeper into debt. Then, if your employer offers a 401(k) match, contribute enough to capture the full match — because that’s an instant return that beats paying off almost any debt. After that, aggressively pay down high-interest debt (anything above 7–8% interest). Once that’s cleared, shift your focus to building a full emergency fund, expanding retirement contributions, and paying down lower-interest debt in parallel. The Dave Ramsey Baby Steps model is one well-known, structured approach to this order if you prefer a clear, step-by-step framework.

Conclusion: Your Budget on a 50K Salary Starts Today

Building a monthly budget on a 50K salary in the US isn’t about deprivation or complicated spreadsheets. Rather, it’s about making thoughtful choices with the money you have — so that over time, you have more options, not fewer.

Your first budget will be imperfect. Your second will be better. By month six, you’ll have a system that fits your actual life, not a generic template from the internet.

Ultimately, the people who succeed financially on a 50K salary aren’t the ones who never treat themselves. They’re the ones who know where their money goes, have a clear plan for saving, and make small, consistent adjustments when life doesn’t cooperate. That’s it — no secret, no shortcut, just a plan.

So start this weekend. Pull up your last two months of bank statements, run the numbers, and pick a budgeting framework. The best time to start your 50K salary budget was last year. The second-best time is right now.