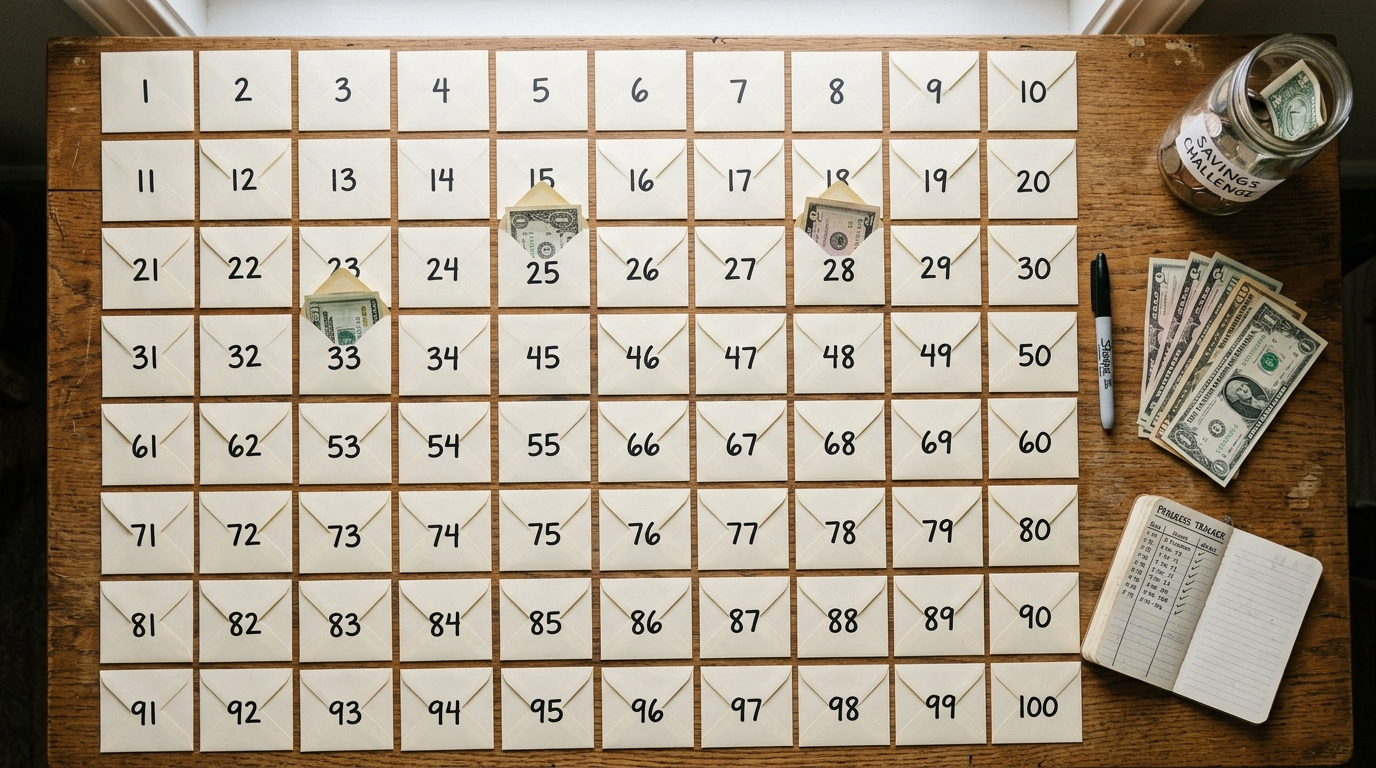

Picture this: a shoebox on your kitchen counter, stuffed with 100 numbered envelopes, slowly filling up with cash you barely noticed leaving your wallet.

By the time the last one is sealed, you’re holding $5,050. No spreadsheet, no app, no willpower-of-steel required.

That’s the promise of the 100 envelope challenge, the cash-stuffing trend lighting up TikTok and savings forums all over again in 2026. But here’s the real question nobody asks loudly enough: does it actually work, or is it just satisfying content to watch?

With rent, groceries, and basically everything else still climbing, people want a way to build savings that feels fast and fun. This challenge delivers on the fun part. The money part depends on a few things creators rarely mention.

So let’s break it down honestly — how it works, what you’ll really save, who it’s perfect for, and the traps that quietly sink most people halfway through.

What the 100 Envelope Challenge Actually Is

At its core, the 100 envelope challenge is almost embarrassingly simple. You grab 100 envelopes and number them 1 through 100.

Each day, you pick an envelope and stuff it with the matching dollar amount. Envelope 1 gets $1. Envelope 47 gets $47. Envelope 100 gets a hundred bucks.

Add every number from 1 to 100 together and you land on $5,050 — saved in just over three months.

The genius isn’t the math; it’s the psychology of turning a vague goal into a tiny daily action you can actually see. Watching that box fill up gives your brain a little hit of progress every single day, which is exactly what keeps most people going.

According to a breakdown from Ramsey Solutions, the appeal is that it gamifies saving — it stops feeling like a chore and starts feeling like a streak you don’t want to break.

It went viral on social media, but the idea isn’t new. It’s the same envelope-and-cash logic your grandparents probably used, just dressed up for the algorithm.

How the 100 Envelope Challenge Works, Step by Step

Ready to actually do it? Here’s the no-fluff version.

- Gather 100 envelopes and a marker. Number each one from 1 to 100. Any cheap pack from the dollar store works fine.

- Toss them into a box or basket — shoebox energy is perfect — and shuffle them so the numbers are hidden.

- Draw one envelope at random each day. Whatever number you pull, that’s the cash you set aside that day.

- Seal it, drop it back in a “done” pile, and repeat for 100 days.

Quick reality check on the rhythm: if you’d rather not gamble, some people fill them in order, $1 on day one up to $100 on day 100. Pulling randomly is more fun but means you might hit a $98 day when money’s tight.

Here’s the thing — you don’t even need physical cash. Plenty of people run a digital version, transferring each amount into a separate high-yield savings account instead.

That digital route is safer (no cash sitting in a box) and your money earns interest along the way. This online approach is often more practical — and your money compounds while you work through the challenge.

Why This Viral Savings Challenge Is Everywhere in 2026

Savings challenges trend in cycles, but the 100 envelope savings challenge has real staying power this year. Why now?

Because saving money has started to feel impossible for a lot of people, and impossible goals don’t get started. A $5,050 target sounds huge — but “put $4 in an envelope today” sounds doable.

That reframe is the whole magic trick. The viral savings challenge of 2026 isn’t winning because it’s clever; it’s winning because it shrinks a scary goal into a daily action your brain says yes to.

There’s also the social side. People film their progress, post their full boxes, and others want in. A money challenge trend spreads fast when it’s this visual and this satisfying.

I know someone who started it purely because a friend kept posting envelope videos. She wasn’t even trying to save for anything specific — she just wanted to see if she could finish. That competitive itch is doing a lot of heavy lifting here.

For Gen Z and millennials especially, it scratches the same itch as a fitness streak or a language-learning app: tangible, trackable, shareable.

Does the 100 Envelope Method Actually Save Money?

Now the honest part. Yes — but with a giant asterisk.

The 100 envelope method absolutely moves money from “spending” to “saved.” If you finish, you’ll have $5,050 you didn’t have before. That’s real.

But spread across 100 days, that’s an average of about $50.50 a day. Over roughly three months, that’s a serious chunk of disposable income — far more than many people can spare without strain.

The challenge doesn’t create money; it just forces you to confront how much you can actually set aside, fast. For some, that’s a wake-up call. For others, it’s a setup for quitting on day 30.

Financial planners are pretty consistent on this: it’s best treated as a short-term motivator — a sprint — not a long-term financial strategy. Consistent budgeting still does more for your future than any 100-day burst.

So does it work? It works as a habit-builder and a confidence boost. It does not replace an actual plan for your money. Think of it as the gateway drug to better saving, not the destination.

Ask yourself honestly before starting: can I realistically part with $50 a day on average right now? If yes, go for it. If no, keep reading — there’s a fix.

5 Mistakes That Quietly Sink the Envelope Challenge

Most people who quit don’t fail because they’re undisciplined. They fail because of avoidable setup mistakes. Here are the big ones.

Mistake 1: Going full-amount when your budget can’t handle it. People copy the $5,050 version because that’s what’s viral, then panic when a $90 envelope lands on a slow week. Fix: scale the amounts down (more on that below).

Mistake 2: Keeping cash loose in a box at home. It’s tempting to “borrow” $20 from envelope 60 for pizza. Fix: deposit into a separate savings account so it’s harder to raid.

Mistake 3: Pulling random envelopes with zero buffer. Randomness is fun until three big numbers hit in a row. Fix: front-load the high envelopes during high-income weeks, or just go in reverse order so the hardest days come early.

Mistake 4: Treating it as your only savings. Pausing your emergency fund or retirement contributions to “win” the challenge is a net loss. Fix: layer it on top of existing habits, not instead of them.

Mistake 5: No plan for the $5,050. Finishing with a pile of cash and no goal often leads straight to spending it. Fix: decide now — debt payoff, emergency fund, a specific purchase — before you start.

How to Make This Cash Savings Challenge Fit Your Real Budget

Here’s where the challenge becomes genuinely useful instead of just aspirational. You can bend the rules without breaking the point.

The most popular tweak: switch from daily to weekly. Fill one envelope per week instead of per day, and the challenge stretches across about two years at a far gentler pace.

Even a small weekly version adds up. Saving around $25 a week lands you near $1,300 by year’s end — meaningful money for an emergency fund.

The best cash savings challenge is the one you’ll actually finish, not the one that looks most impressive on camera. A completed $1,300 beats an abandoned $5,050 every time.

Other ways to right-size it: halve every amount to target ~$2,525, cap your envelopes at 50, or set a fixed monthly ceiling and only pull envelopes you can cover.

A friend of mine ran the half-version through last winter, parked it all in a high-yield account, and used it to cover holiday spending in cash — zero credit card debt in January for the first time ever. That’s the kind of win that compounds into better habits.

The structure is the gift here. Whether you save $1,300 or $5,050, you’re training the muscle that matters: paying yourself first, consistently. This pairs naturally with a sinking fund for predictable irregular expenses — once the challenge is done, the habit is already there.

How It Stacks Up Against Other Money Challenges

The 100 envelope challenge isn’t the only money challenge trend making the rounds. If you’re shopping for the right fit, it helps to see how it compares.

The save money fast challenge crowd usually loves the envelope method precisely because of its speed — $5,050 in three months is hard to beat for sheer momentum. Few other gamified methods front-load results that aggressively.

But speed cuts both ways. Compare it to gentler options and the trade-offs get clearer.

The 52-week challenge asks for $1 in week one, $2 in week two, on up to $52 — totaling $1,378 over a full year. Slower, but almost painless and easy to sustain.

The 365-day penny challenge is the marathon: a penny on day one, two cents on day two, ending the year around $667. Tiny amounts, big patience required.

No-spend challenges flip the script entirely — instead of stashing cash, you simply stop discretionary spending for a set stretch and let the savings come from what you didn’t buy.

Here’s the honest comparison: the envelope challenge wins on motivation and visible progress, but loses on flexibility for tight or irregular incomes. If your paycheck swings month to month, a flat weekly amount or a no-spend week may stick better. If you’re working with a tight monthly income, even the scaled-down version can make a real dent.

The smart move? Many people run the envelope challenge first for the dopamine, then graduate to a steadier monthly system like a zero based budget once the saving habit feels automatic. Use the trend as a launchpad, not a finish line.

Final Thoughts: Should You Try It in 2026?

Remember that shoebox on the counter? By now you can probably see it for what it really is — not a magic money machine, but a clever nudge that makes saving feel like a game you want to win.

The 100 envelope challenge won’t fix a tight budget or build wealth on its own. What it will do is turn an abstract goal into 100 small, satisfying wins, and that shift in mindset is worth more than the cash for a lot of people.

If you’ve got the room, run the full $5,050 sprint. If you don’t, scale it down with zero guilt — a finished smaller challenge beats a heroic one you ditch in week four.

Either way, set your goal before you number a single envelope, keep the money somewhere you can’t easily raid, and treat it as a stepping stone toward a real budget. Pair the challenge with the 50/30/20 rule to keep the rest of your finances in order while you sprint.

Pick your version, grab those envelopes, and fill envelope number one today. Future-you will be glad you did.

Frequently Asked Questions

Q: How much do you save with the 100 envelope challenge?

You save $5,050 if you complete the full version, since that’s the sum of every number from 1 to 100. Scaled versions save less — a weekly or half-amount approach typically lands between $1,300 and $2,525. Pick the target you can realistically finish.

Q: Is the 100 envelope challenge actually a good way to save money in 2026?

It’s a great motivator and habit-builder, especially if you struggle to start saving. But financial experts treat it as a short-term sprint, not a long-term plan, so pair it with a regular budget and a high-yield savings account for the best results.

Q: Can I do the 100 envelope savings challenge without physical cash?

Yes. Many people run it digitally by tracking numbers on a printable or spreadsheet and transferring each amount into a separate savings account. This is safer than storing cash at home and lets your money earn interest while you go.

→ Related: How to Live on $1,500 a Month: 7 Real Steps for 2026