You opened your banking app, saw the number, and felt your stomach drop. Again.

It wasn’t one big purchase. It was the $7 coffees, the “treat yourself” cart on a bad day, the third food delivery this week. Death by a thousand taps.

If that hits a nerve, you’re not broken — and you’re definitely not alone. One in four Americans tried a no-spend reset this year, and the no spend challenge rules below are exactly what turns a vague “I should save more” into a plan that actually works.

Here’s the thing: most people quit by day nine. Not because they’re weak, but because nobody told them the rules upfront. They wing it, slip once, feel like a failure, and bail.

This guide fixes that. You’ll get the real rules, the daily-life loopholes that trip everyone up, and a survival plan for when the cravings hit. Let’s reset your money — for good.

What a No Spend Challenge Actually Is (and the Core Rules)

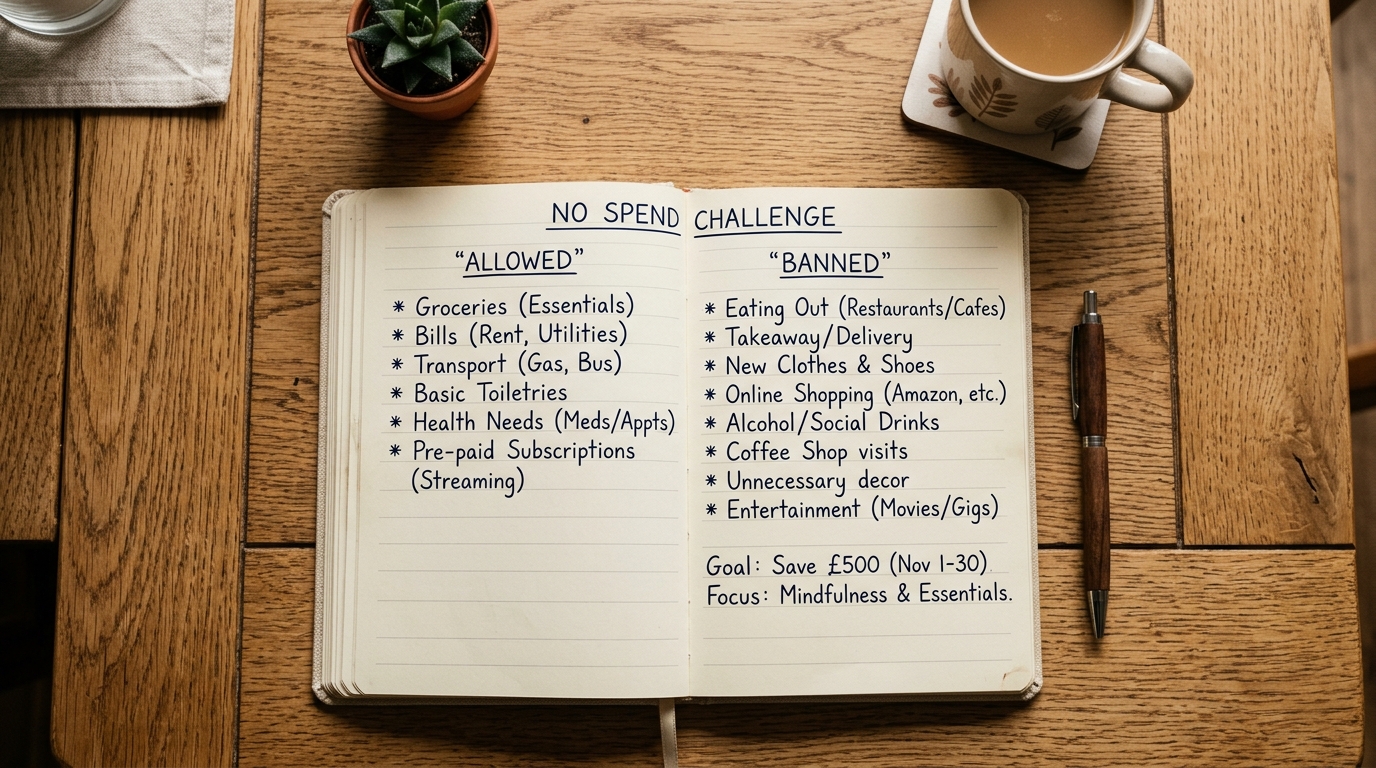

A no-spend challenge is a set period where you pause all non-essential spending. Rent, groceries, utilities, medicine, transport — those stay. Everything else gets frozen.

The catch is that “everything else” is fuzzy until you write it down. That’s why the no spend challenge rules matter more than willpower.

Before day one, you split your money into two lists: Allowed and Banned — and you do it in writing, not in your head.

Allowed usually covers: rent or mortgage, utilities, groceries (real food, not snacks-as-meals), gas or transit, insurance, medical needs, and minimum debt payments. Banned usually covers: takeout, coffee runs, clothes, gadgets, beauty products, subscriptions you forgot about, and “I’ll just browse” online shopping.

A friend of mine, Maya, started a no-spend month and forgot to define “groceries.” By day four she was buying $12 artisan cheese and calling it dinner. Define your line, or your brain will redraw it for you.

Why the No Spend Challenge Is Exploding in 2026

This isn’t a niche frugal-blogger thing anymore. It’s everywhere.

Searches for “No Buy January” hit a five-year high heading into 2026, and a NerdWallet survey of around 2,000 people found one in four had attempted a no-spend challenge, with 12% doing one this January.

So why now? Three forces collided.

First, inflation fatigue — five-ish years of prices climbing while paychecks crawl. Second, lifestyle creep: the more you earn, the more “normal” expensive habits feel. Third, AI-driven job anxiety, which makes people grip tighter to the things they can control.

A report cited by the Wall Street Journal noted the trend is driven mostly by Gen Z and millennials sharing their spending rules and progress online. One Reddit no-buy community alone has crossed 70,000 members trading tips and wins.

Translation? You’re joining a movement, not punishing yourself. And that social momentum is a quiet superpower when motivation dips.

The 7 No Spend Challenge Rules That Actually Work

Here’s the framework. Follow these and you’ll outlast the day-nine quitters by a mile.

- Pick a realistic length first. A no spend week challenge is the perfect on-ramp — short enough to win, long enough to feel it. Graduate to a month once you’ve proven you can.

- Write your Allowed and Banned lists before you start. Vague rules are broken rules. Tape the list somewhere you’ll see it daily.

- Set a single “why” you can repeat out loud. “I want $600 toward my emergency fund” beats “I should save.” Specific goals survive bad days.

- Build one guilt-free exception. Maybe one $15 social outing a week. Total restriction backfires — a small valve stops the whole thing from exploding.

Quick scenario: Jordan tried a no-spend month with zero exceptions, white-knuckled it for eight days, then blew $90 on a single Friday out of pure rebellion. A planned exception would’ve cost him $15 and saved the whole month.

- Track every dodged temptation. Each time you almost buy something and don’t, jot the amount. Watching “money I didn’t spend” climb is weirdly addictive — in a good way.

- Remove the friction that makes you spend. Delete saved cards, log out of shopping apps, unsubscribe from sale emails. Make impulse buying a hassle, not a reflex.

- Plan free replacements for your spending triggers. Bored? Library, walk, that hobby you abandoned. The goal isn’t an empty month — it’s a full one that doesn’t cost anything.

These no spend challenge rules work because they remove decisions, not just dollars — and decision fatigue is what actually breaks people.

No Spend Week Challenge vs. No Spend Month: Which to Pick

Not sure how long to commit? Start with the math of your own willpower.

A no spend week challenge is the smart first move. It’s basically a spending detox sprint — you can grit through almost anything for seven days, and the early win builds belief.

Want more no spend month tips? The month version needs structure the week doesn’t. Plan your meals in advance, batch-cook, and warn your friends so they stop inviting you to brunch you’ll have to decline.

I know what you’re thinking — “a whole month sounds miserable.” Here’s the surprise most people report: by week two, the cravings fade and the savings start feeling like a game you’re winning.

If a full month feels like too much, try a “low-buy” month instead: not zero spending, just strict limits on one or two problem categories. Many people doing the no buy challenge 2026 actually run a low-buy version and still save hundreds.

Related: How to Set Up Sinking Funds — a great way to bank your no-spend savings into targeted goals once the challenge ends.

Spending Freeze Rules: The Daily-Life Loopholes Nobody Warns You About

This is where good intentions go to die. The official spending freeze rules are easy; real life is sneaky.

The “it was on sale” trap. A discount on something you weren’t going to buy isn’t saving — it’s spending with a story attached. During a freeze, a deal is still a banned purchase.

The gift-card dodge. Using a gift card to buy banned stuff still breaks the challenge mentally. The point is the habit, not the dollars.

The “someone else paid” blur. If you keep nudging friends to cover you, you’re not doing the challenge — you’re outsourcing it. Be honest with yourself.

The restock loophole. “I’m almost out of moisturizer” turns into a $60 beauty haul. Replace essentials only when they’re truly empty, and only the item itself.

The boredom buy. This is the big one. Most impulse spending isn’t about need — it’s about mood. Catch the feeling, name it, then do your free replacement instead.

Spot which one is your personal kryptonite now, before it ambushes you on day six.

How to Survive the Hard Days (Your Money Reset Challenge Toolkit)

Every money reset challenge has a wall. Usually it shows up around day seven to ten, when novelty wears off and life gets stressful.

Here’s your toolkit for pushing through.

Use the 48-hour rule. Want something banned? Write it down and wait two days. Most urges evaporate. The ones that don’t are probably real needs you can plan for later.

Lean on the community. Post your progress, read others’ wins, ask for a pep talk. That 70,000-member momentum exists for exactly these moments.

Reframe the discomfort. That itch to spend? It’s a habit loop firing, not an emergency. Naming it (“ah, there’s my 9pm boredom craving”) drains its power fast.

Stack tiny rewards that aren’t purchases. Finished a hard day? A long bath, a favorite playlist, an episode of your show. Reward the streak without breaking it.

Keep your “why” visible. That $600 goal, that debt you’re killing, that trip you’re funding. Put it on your lock screen so it’s the first thing you see when the temptation app calls.

One more honest note: if you slip, you didn’t fail the whole challenge. You had one bad hour. Reset and keep going — perfection was never the rule.

A Real No-Buy Story: What 30 Days Actually Saved

Let me make this concrete with someone real-ish — a composite of the stories you’ll find all over the no buy challenge 2026 communities.

Call her Priya. Twenty-eight, decent salary, and somehow always broke by the 25th. Her leak wasn’t rent; it was the $40-a-week food delivery, the impulse skincare, and the “I deserve it” weekend hauls.

She didn’t go scorched-earth. She set simple no spend challenge rules: groceries and bills allowed, one $20 social outing a week as her planned exception, everything else frozen for 30 days.

Week one was rough — she nearly caved on day six during a stressful evening. The 48-hour rule saved her; the urge was gone by morning. Week two, she started cooking again and actually enjoyed it.

By day 30, she’d held back roughly $480 she would’ve otherwise spent on autopilot. But the bigger win was the realization underneath it: most of her spending had nothing to do with wanting things. It was stress, boredom, and habit wearing a shopping disguise.

The lesson isn’t that Priya saved $480 — it’s that she found her real spending triggers, which is the thing that keeps the savings going long after the challenge ends.

That’s the quiet payoff of these spending freeze rules. The money is nice. The self-knowledge is what lasts.

Final Thoughts: Your Reset Starts With One Rule

Remember that stomach-drop moment when you opened your banking app? That feeling came from a hundred decisions made on autopilot.

A no-spend challenge isn’t about deprivation. It’s about taking the wheel back — proving to yourself that you decide where your money goes, not the algorithm, the sale email, or the 9pm boredom. The no spend challenge rules here aren’t chains; they’re guardrails that make the road easier.

You don’t have to overhaul your life tonight. Pick one rule. Write your Allowed and Banned lists, or just commit to a no spend week challenge starting tomorrow.

Small win first. Momentum second. Real change after that.

Save this post, screenshot the seven rules, and start your reset this week — your future self, checking that banking app with a smile, will thank you.

Related: Zero Based Budgeting for Beginners — pair your no-spend reset with a proper budget to lock in the savings you’ve built.

Frequently Asked Questions

Q: What are the basic no spend challenge rules for beginners?

Pause all non-essential spending for a set time while keeping essentials like rent, groceries, and bills. Write a clear “Allowed” and “Banned” list before you start, set one specific savings goal, and build in one small planned exception so you don’t burn out. Start with a week before attempting a month.

Q: How long should a no spend challenge last?

Beginners should start with a no spend week challenge, then graduate to two weeks or a full month once they’ve had a win. The length matters less than finishing — a completed week beats an abandoned month every time. Many people doing the no buy challenge 2026 run repeating monthly resets rather than one long stretch.

Q: What counts as essential during a spending freeze?

Essentials are things you genuinely need to live and function: housing, utilities, groceries, transport, insurance, medication, and minimum debt payments. Everything discretionary — takeout, clothes, gadgets, subscriptions, impulse buys — gets paused. The trap is letting “essential” quietly expand, so define your line in writing before day one.

→ Related: No Buy Year Rules: 7 Honest Steps to Save Big in 2026

→ Related: 12 Proven Free Weekend Ideas to Save Big in 2026

→ Related: How to Stop Spending Money: 9 Proven Habits That Finally Work in 2026

")