Learning how to save $1000 a month on a $60,000 salary is one of the smartest financial moves you can make — and it is far more achievable than most people think. Thousands of Americans at this exact income level hit this target every month. That said, it does require a real plan, honesty about where your money goes, and a willingness to make a few intentional changes.

In this guide, you’ll find a clear, step-by-step breakdown of exactly how to save $1000 a month on a $60K income. We cover budgeting methods, the biggest spending categories to target, automation tricks, and side income strategies. By the end, you’ll have everything you need to start this month.

Before we dive in, however, let’s get grounded in the math — because understanding your actual take-home pay is the foundation of everything that follows.

What $60K Actually Looks Like After Taxes (The Starting Point)

To successfully save $1000 a month, you first need to know what you’re working with. Your gross salary and your take-home pay are two very different numbers, and most people underestimate the gap.

On a $60,000 annual salary in the U.S., federal income tax places you in the 22% marginal bracket. After federal taxes, Social Security (6.2%), and Medicare (1.45%), your federal deductions typically remove $12,000–$14,000 per year. If you live in a state with income tax — California takes close to 6%, while states like Texas and Florida take zero — your actual take-home lands somewhere between $42,000 and $47,000 annually.

That works out to roughly $3,500–$3,900 per month in your pocket. For the purposes of this guide, we’ll use $3,700 as our working number throughout.

💡 Quick Math: If your take-home is $3,700/month and your goal is to save $1,000 of it, that means living intentionally on $2,700. Tight? Yes. But it’s entirely doable with the right structure.

Step 1: Build the Right Budget to Save $1000 a Month

Most people who struggle to save $1000 a month aren’t spending carelessly — they’re simply spending without a plan. So the money disappears before the month ends, leaving savings as an afterthought rather than a priority.

The solution is a forward-looking budget — one you build before the month begins, not a spending tracker you fill in after the damage is done.

The 50/27/23 Split for a $60K Salary

The classic 50/30/20 rule is a useful starting point. However, to genuinely save $1000 a month on $3,700 take-home, you need to adjust the proportions slightly:

- Needs (housing, utilities, groceries, transport, insurance): 50% = ~$1,850

- Wants (dining out, subscriptions, entertainment, clothing): 23% = ~$850

- Savings + debt payoff: 27% = ~$1,000

That 27% target is your number. And it still leaves $850/month for discretionary spending — so this isn’t a joyless existence.

Budgeting Tools That Help You Stay on Track

You don’t need an elaborate system. In fact, the simpler, the better. Here are three tools people at this income level use successfully:

- YNAB (You Need a Budget) — assigns every dollar a specific job before it’s spent. At $14.99/month, users report saving an average of $600 more in their first two months. Visit YNAB.com to get started.

- The envelope method — cash in labeled envelopes for each spending category. It’s old-school, but psychologically powerful because physical cash feels more real than a card swipe.

- A simple Google Sheet — two columns: planned income, planned expenses. Update it weekly. Nothing fancy required.

For more on building a household budget, the Consumer Financial Protection Bureau offers a free interactive tool.

Step 2: Attack the Big Three Expenses First

Here’s what most budgeting articles get wrong: they focus on small cuts like skipping your morning coffee. But the fastest path to $1,000 a month runs through your three largest spending categories — housing, transportation, and food. Together, these typically consume 60–70% of most Americans’ budgets. Therefore, moving the needle here moves it everywhere.

Housing: Your Biggest Financial Lever

According to the U.S. Bureau of Labor Statistics, Americans spend an average of 33% of their after-tax income on housing. On a $60K salary, that’s close to $1,000/month just on rent or mortgage — which leaves very little room to save $1000 a month elsewhere.

- House hacking — renting a spare room can bring in $400–$700/month. Your effective housing cost drops dramatically without you moving at all.

- Refinancing your mortgage — a 1% rate reduction on a $200K balance saves approximately $120/month.

- Relocating within your metro — moving one ZIP code away from a trendy neighborhood frequently saves $200–$400/month in rent with no lifestyle change.

Transportation: The Hidden Money Pit

The average American spends about $10,742 per year on vehicle ownership, according to AAA’s annual driving costs study. That’s nearly $900/month when you combine car payments, insurance, fuel, and maintenance.

- Refinance your auto loan if your credit score has improved — dropping from 8% to 5% on a $20K balance saves roughly $50/month.

- Shop car insurance every year. Drivers who compare quotes annually save an average of $400–$700/year. Bundling with renters insurance often reduces costs further.

- In walkable cities, going down to one car per household can free up $300–$500/month instantly.

Food: The Category with the Most Immediate Flexibility

Groceries and restaurants together average $500–$800/month for a single person or couple. Restaurant spending is the easier target — and the most rewarding one to tackle first.

- Meal prepping on Sundays reduces weekly food costs by 30–40% for most households.

- Switching from a premium grocery chain to ALDI or Lidl saves the average family $150–$200/month with nearly identical nutritional outcomes.

- The “eat before you shop” rule sounds simple because it is — and it works consistently.

📌 Real Example: Maria, a 28-year-old teacher in Austin earning $58,000, cut her monthly restaurant spending from $340 to $120 by meal prepping three times a week and using Flashfood for discounted near-expiry groceries. That single change freed up $220/month — nearly a quarter of her savings goal.

Step 3: Cut Subscriptions to Save $1000 a Month Faster

A 2023 study by C+R Research found that Americans underestimate their monthly subscription spending by an average of $133. The average person actually spends $219/month on subscriptions — streaming services, gym memberships, apps, meal kits, and software they’ve simply forgotten about.

Set aside 30 minutes this week for a subscription audit:

- Pull up your last two bank and credit card statements.

- Highlight every recurring charge.

- For each one, honestly ask: “Did I use this at least three times last month?”

- Cancel everything that fails that test.

Streaming services alone add up fast. For instance, if you subscribe to Netflix, Hulu, Disney+, HBO Max, and Spotify simultaneously, you’re spending $60–$80/month. Rotating services — using one for two months, canceling, then trying another — is an easy workaround that preserves access without the full cost.

Step 4: Reduce Your Phone and Utility Bills Without Sacrifice

Utility and phone bills feel fixed to most people. In reality, they’re almost always negotiable or reducible — and the savings here require very little ongoing effort once you set them up.

Phone Bill: Switch Carriers, Keep the Network

The average American pays $127/month for a phone plan. Switching to an MVNO like Mint Mobile, Visible, or Consumer Cellular — all of which operate on the same major carrier networks — cuts that to $25–$45/month. That’s a potential $80/month saved from a single decision.

Internet: The Retention Call That Pays Off

Call your internet provider and ask directly about retention offers or loyalty discounts. This works with surprising frequency. Most providers maintain unpublished rates for customers who ask. A 10-minute call typically saves customers $20–$40/month.

Energy: Set-It-and-Forget-It Savings

The U.S. Department of Energy estimates smart thermostats save homeowners around $180/year. Add LED bulbs throughout your home (roughly $75/year in additional savings) and you’ve effectively covered a tank of gas each month without changing a single daily habit.

Step 5: Automate Your Savings So You Actually Save $1000 a Month, Every Month

The single most effective strategy to save $1000 a month has nothing to do with cutting spending. Instead, it’s making saving automatic. When your bank transfers $1,000 to a savings account the day after your paycheck lands, you never see it sitting in checking. You never make the decision to spend it. It’s simply allocated before you have the chance.

- Schedule an automatic transfer in your bank’s app for the day after your direct deposit arrives.

- Use a high-yield savings account (HYSA) — banks like Marcus, Ally, and SoFi currently offer 4.5–5% APY, compared to the national average of 0.46%.

- If your employer offers 401(k) matching, contribute at least enough to capture the full match. A $60K earner contributing 5% ($250/month) to receive a 3% employer match earns an additional $150/month in free compensation.

💬 The “Pay Yourself First” principle — popularized by David Bach’s The Automatic Millionaire — is the behavioral foundation of most successful savings stories. Automation removes the willpower requirement entirely, which is why it succeeds where manual saving often fails.

Step 6: Earn More to Make It Easier to Save $1000 a Month

Sometimes cutting expenses isn’t enough — particularly in high cost-of-living areas. In that case, a modest side income bridges the gap and makes saving $1000 a month feel genuinely comfortable rather than like a constant struggle.

- Freelance your current skills — writing, design, bookkeeping, coding, social media management. Platforms like Upwork and Fiverr make it easy to find initial clients.

- Sell unused household items — the average American household contains $3,000–$5,000 in unused belongings. Facebook Marketplace and eBay convert clutter into capital quickly.

- Gig work on weekends — DoorDash, Instacart, or TaskRabbit. Even 4–5 hours on a Saturday typically nets $60–$100.

- Pet sitting or dog walking through Rover — one of the most pleasant side incomes available, with some part-time sitters earning $500–$800/month.

Step 7: Restructure Your Debt (It’s Quietly Killing Your Savings)

High-interest debt is the most overlooked obstacle to saving money each month. Carrying $5,000 on a credit card at 22% APR costs approximately $91/month in interest alone — money that benefits only the bank.

The Avalanche Method

List your debts from highest interest rate to lowest. Pay minimums on everything except the top one, directing every spare dollar there. Once it’s eliminated, roll that payment toward the next debt. This approach minimizes total interest paid over time.

The Snowball Method

List debts from smallest balance to largest. Pay off the smallest first for psychological momentum. Although not the most mathematically efficient, the behavioral benefit is real — quick wins keep people motivated to continue.

Balance Transfers and Consolidation Loans

If your credit score exceeds 680, you may qualify for a 0% APR balance transfer card (12–21 months interest-free) or a debt consolidation loan at 8–12%. Either option is dramatically better than 22%+ credit card rates and can free up $50–$150/month on a moderate balance.

Step 8: Small Daily Habits That Add Up to Big Monthly Savings

This step isn’t about eliminating joy. Rather, it’s about spending intentionally — making conscious choices instead of automatic ones.

The 48-Hour Rule

For any non-essential purchase over $50, wait 48 hours before buying. Research shows roughly 70% of impulse buying urges disappear within two days. Therefore, this single rule can prevent $100–$300 in unnecessary monthly spending.

Cash-Back Apps on Existing Purchases

Apps like Rakuten, Ibotta, and Fetch Rewards return $20–$50/month on groceries and shopping you’re already doing. Since there’s no behavior change required, this is purely additive savings.

Coffee at Home on Weekdays

At $5 per coffee shop visit, five days a week adds up to $100/month — or $1,200/year. A quality pour-over setup costs $30 one-time. Plenty of people end up preferring home-brewed coffee once they dial in the recipe.

Borrow Before You Buy

Library cards now include free ebooks and audiobooks through the Libby app, as well as museum passes in many cities. Before purchasing a book, course, or tool, check your local library first. A surprising amount of what you were about to buy is sitting there free.

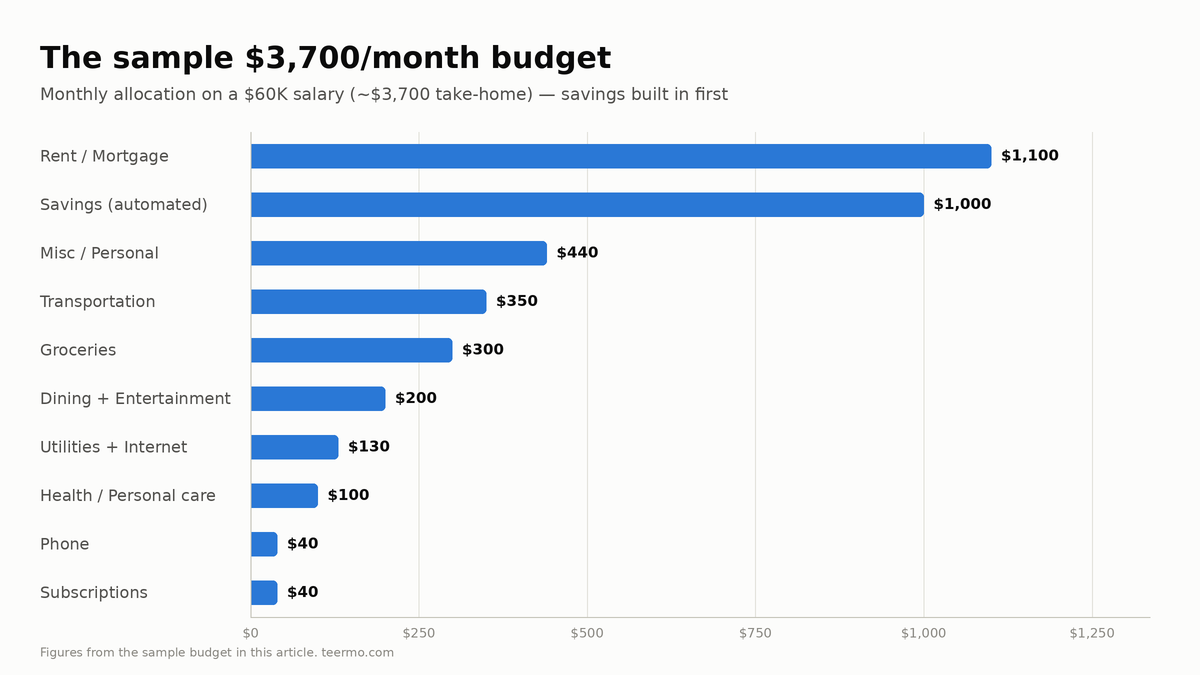

Putting It All Together: A Sample $3,700/Month Budget

| Category | Monthly Amount |

|---|---|

| Rent / Mortgage | $1,100 |

| Utilities + Internet | $130 |

| Groceries | $300 |

| Transportation (car + gas + insurance) | $350 |

| Phone | $40 |

| Health / Personal care | $100 |

| Subscriptions (curated) | $40 |

| Dining out + Entertainment | $200 |

| Miscellaneous / Personal | $440 |

| Savings (automated transfer) | $1,000 |

| TOTAL | $3,700 |

These numbers reflect what real people earning similar incomes across mid-sized American cities actually live on. Rent at $1,100 requires either living outside a major metro, sharing housing, or house hacking. In expensive cities like New York or San Francisco, the target may shift to $700–$800/month initially. The principles stay the same either way.

How Long Before You Notice a Real Difference?

Month one is always the hardest. Nevertheless, most people find that by month two or three, the budget starts feeling natural. The automated savings become background noise. The new habits feel normal.

By month six, you have $6,000 saved. By month twelve, $12,000 — a full emergency fund for most people at this income level. It means car repairs don’t derail your budget, medical bills don’t go on credit cards, and you gradually stop living paycheck to paycheck — not because you earned more, but because you built a working system.

Frequently Asked Questions

Is it realistic to save $1000 a month on a $60,000 salary?

Yes — and many Americans do it successfully. It requires intentional budgeting and some lifestyle adjustments, but $1,000/month represents approximately 27% of a typical $3,700 take-home on a $60K salary. The key factors are keeping housing costs at or below 30% of take-home, reducing discretionary spending, and automating the savings transfer so the money is allocated before you can spend it.

What’s the fastest way to save $1000 a month if I’m just starting out?

Focus on your three biggest expenses first — housing, transportation, and food. These together typically account for 60–70% of most budgets. Getting a roommate, shopping your car insurance, and reducing restaurant spending can collectively free up $500–$700/month relatively quickly. And automating your savings transfer means the money is saved before it can be spent.

Should I save $1000 a month or pay off debt first?

It depends primarily on the interest rate. For high-interest debt (credit cards at 15%+), paying it down first delivers a guaranteed return equal to the interest rate. For low-interest debt (student loans at 4–6%), building a $1,000 emergency fund first is generally wiser. After that, split additional funds between debt payoff and savings simultaneously.

What if I live in an expensive city and saving $1000 a month isn’t feasible?

Adjust the goal proportionally. In San Francisco or New York City, $600–$800/month may be a more realistic ceiling on a $60K income. Prioritize building a $1,000 emergency fund first, then build toward the full $1,000/month as income grows. Increasing income through side work is often more effective in high cost-of-living cities than cutting spending further.

How do I stay motivated to save $1000 a month consistently over the long term?

Tie your savings to a specific, visible goal — not “save money,” but “buy a house in three years” or “take a trip to Japan.” Research consistently shows named, concrete savings goals drive more consistent behavior than abstract targets. Many high-yield savings accounts let you name sub-accounts — watching “Europe Trip 2026” grow each month is far more motivating than a generic number.

Final Thoughts: Your Plan to Save $1000 a Month Starts Today

Saving $1,000 a month on a $60,000 salary is genuinely achievable — not through deprivation, but through intention. It requires a real budget, strategic cuts in the right categories, automation that removes willpower from the equation, and the willingness to find smarter options instead of habitual ones.

The Americans who do this successfully aren’t exceptional earners. They’re people who decided their financial future mattered enough to build a working system around it. They stopped leaving their savings up to chance.

Start with one change this week. Cancel one subscription, set up that automatic transfer, or prep your lunches for the next five days. Momentum builds from small wins. Your $12,000 — and the financial breathing room that comes with it — is one good month away from getting started.

")

1 Comment

There’s certainly a lot to learn about this issue. I love all the points you’ve made.